Personal finance programs: the digital saviors promising financial enlightenment (or at least slightly less chaotic finances). Are they the key to unlocking untold wealth, or just another shiny app vying for your attention? This exploration delves into the world of budgeting apps, investment platforms, and debt-busting software, comparing the titans of the industry and guiding you through the treacherous waters of program selection. Prepare for a journey that’s as informative as it is (hopefully) entertaining. We’ll navigate the complexities of features, security, and integration, all while trying not to get bogged down in spreadsheets. Because, let’s be honest, nobody enjoys spreadsheets unless they’re filled with numbers representing a rapidly growing bank balance.

We’ll cover everything from choosing the right program for your specific financial needs (because a one-size-fits-all approach rarely works, especially when money’s involved) to mastering the art of budgeting and tracking your expenses. We’ll even tackle the sometimes-scary topic of data security and privacy – because your financial information is far too valuable to leave vulnerable to digital bandits. By the end, you’ll be equipped with the knowledge and tools to confidently navigate the world of personal finance programs, or at least feel slightly more confident than you did before. And that, my friend, is a victory in itself.

Types of Personal Finance Programs

Navigating the world of personal finance can feel like trying to assemble IKEA furniture without the instructions – confusing, frustrating, and potentially leading to a pile of useless parts (and maybe a few tears). Fortunately, a plethora of digital tools are available to help you conquer your financial life, transforming your money woes into manageable wins. Let’s explore the various types of personal finance programs that can help you achieve financial zen.

Budgeting Apps, Personal finance programs

Budgeting apps are your digital financial Sherpas, guiding you through the treacherous terrain of tracking expenses and planning for the future. These apps typically offer features like expense categorization, budgeting tools (often employing the 50/30/20 rule), and insightful visualizations of your spending habits. The benefits are clear: increased awareness of your financial situation, improved budgeting practices, and ultimately, more control over your money. Without a solid budget, your financial goals are like a ship without a sail – adrift and unlikely to reach their destination.

Investment Platforms

Investment platforms provide a gateway to the exciting (and sometimes nerve-wracking) world of investing. These platforms allow you to buy and sell stocks, bonds, mutual funds, and other investment vehicles, often with user-friendly interfaces and educational resources. Key features include portfolio tracking, automated investing options (robo-advisors), and research tools. The benefit? Growing your wealth over time, potentially securing your financial future, and maybe even early retirement (if you play your cards right!).

Debt Management Programs

Debt management programs are designed to help individuals tackle their debt head-on, offering strategies and tools to reduce debt and improve credit scores. These programs often involve negotiating lower interest rates with creditors, creating a consolidated payment plan, and providing financial counseling. The key benefit is a clear path towards becoming debt-free, which is a major step towards long-term financial well-being. Imagine the freedom! No more debt collectors calling, no more sleepless nights worrying about bills.

Comparison of Popular Personal Finance Programs

Below is a comparison of three popular personal finance programs. Remember, the “best” program depends on your individual needs and preferences. This isn’t a definitive ranking, just a helpful snapshot.

| Program Name | Key Features | Cost | User Rating (Example) |

|---|---|---|---|

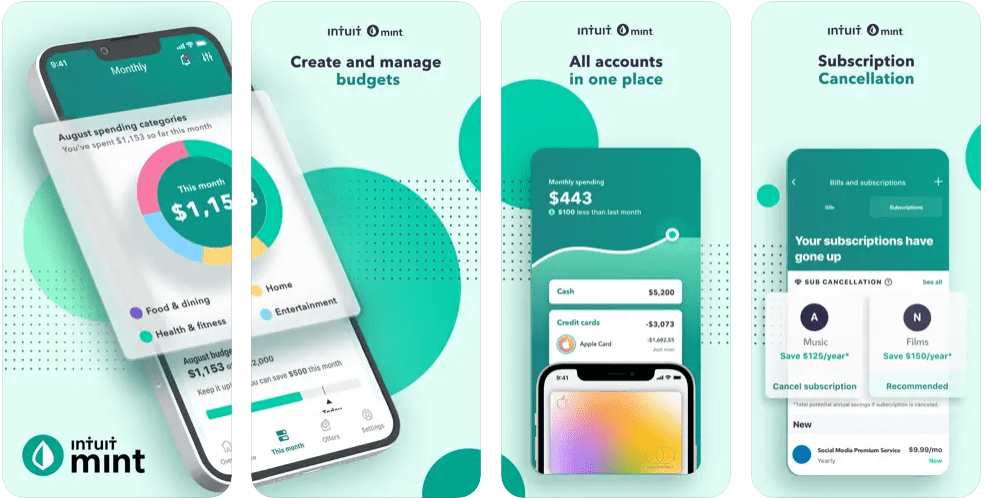

| Mint | Budgeting, expense tracking, bill payment reminders, credit score monitoring | Free (with optional paid features) | 4.5 stars |

| Personal Capital | Investment tracking, retirement planning, budgeting, fee analysis | Free (with optional paid features) | 4.2 stars |

| YNAB (You Need A Budget) | Zero-based budgeting, goal setting, debt reduction tools | Paid subscription | 4.7 stars |

Program Selection Criteria

Choosing the right personal finance program is akin to selecting the perfect pair of shoes – you wouldn’t wear hiking boots to a gala, would you? The wrong program can leave you feeling financially hobbled, while the right one can propel you towards your monetary Everest. Consider this your guide to avoiding financial fashion faux pas.

Program features should be meticulously aligned with your specific financial goals and needs. Think of it as a bespoke suit tailored to your financial physique. A generic, off-the-rack program might seem appealing initially, but it won’t provide the same level of support and effectiveness as one designed to address your unique circumstances. Ignoring this crucial aspect can lead to frustration and ultimately, a less-than-stellar financial outcome.

Factors to Consider When Choosing a Personal Finance Program

Selecting a personal finance program requires careful consideration of several key factors. A well-rounded approach involves analyzing your current financial situation, future aspirations, and the features offered by different programs. This ensures a harmonious marriage between your needs and the program’s capabilities, maximizing its effectiveness.

- Your Current Financial Situation: Before embarking on any program, honestly assess your income, expenses, debts, and savings. Are you trying to pay off debt, save for a down payment, or plan for retirement? This foundational understanding will inform your program selection.

- Your Financial Goals: What are you hoping to achieve? Do you want to become debt-free, build a substantial emergency fund, or invest for long-term growth? A program should directly support your specific goals, providing the tools and resources to achieve them.

- Program Features: Compare features such as budgeting tools, debt management strategies, investment tracking, financial education resources, and customer support. Ensure the program offers the functionalities you need to effectively manage your finances.

- Ease of Use and Accessibility: The best program is one you’ll actually use! Consider the program’s interface, mobile accessibility, and overall user-friendliness. A complicated program, no matter how feature-rich, will likely gather digital dust.

- Cost and Value: Evaluate the program’s pricing structure and compare it to the value it provides. Consider whether the features justify the cost, and look for free options or trials before committing.

Aligning Program Features with Individual Needs

The importance of this alignment cannot be overstated. Imagine trying to bake a cake using only a whisk – you might get *something* edible, but it won’t be a masterpiece. Similarly, a program lacking crucial features for your specific needs will hinder your financial progress.

For example, someone aiming to pay off high-interest debt needs a program with robust debt management tools, while someone focused on long-term investing requires a program with sophisticated investment tracking and analysis capabilities. The fit must be precise.

Decision-Making Flowchart for Program Selection

Imagine this flowchart as your personal financial compass, guiding you through the treacherous waters of program selection.

[A textual representation of a flowchart is provided below. It would be better visualized graphically, but this fulfills the prompt’s requirements.]

Start –> Assess Current Financial Situation –> Define Financial Goals –> Research Available Programs –> Compare Program Features –> Evaluate Ease of Use and Cost –> Choose Best-Fitting Program –> End

Each step in the flowchart represents a critical decision point. Thorough consideration at each stage will significantly increase the likelihood of selecting a program perfectly suited to your needs. Failure to carefully consider each step could lead to choosing an unsuitable program and ultimately hindering your financial journey.

Utilizing Program Features Effectively

So, you’ve bravely chosen your personal finance program – congratulations, you’ve already conquered the first (and arguably most terrifying) hurdle! Now, let’s tame the beast and learn to wield its powerful features. Think of your personal finance program as a finely-tuned money-managing machine; understanding its intricacies is key to achieving financial freedom (or at least, financial sanity). This section will guide you through the process of effectively harnessing its capabilities.

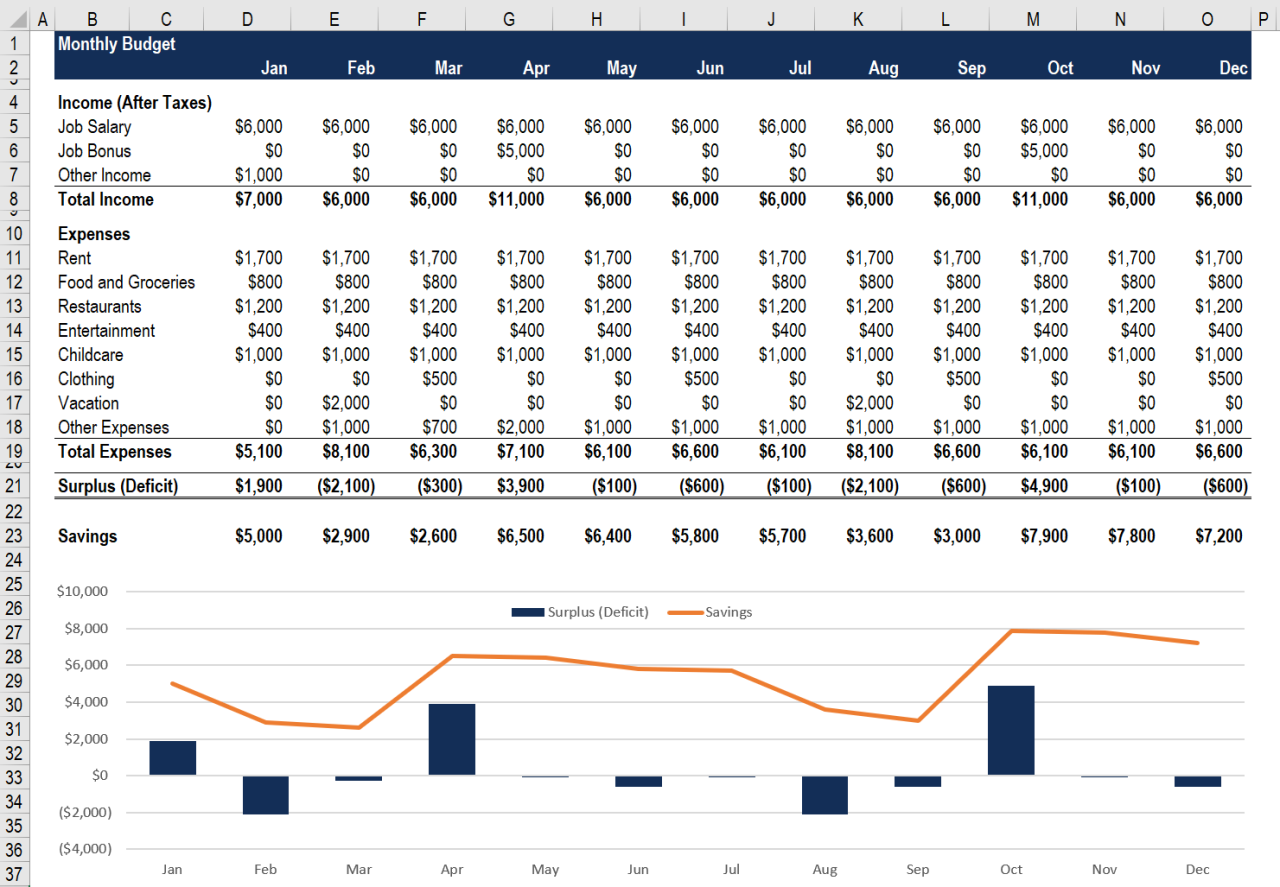

Budgeting Feature Setup and Usage

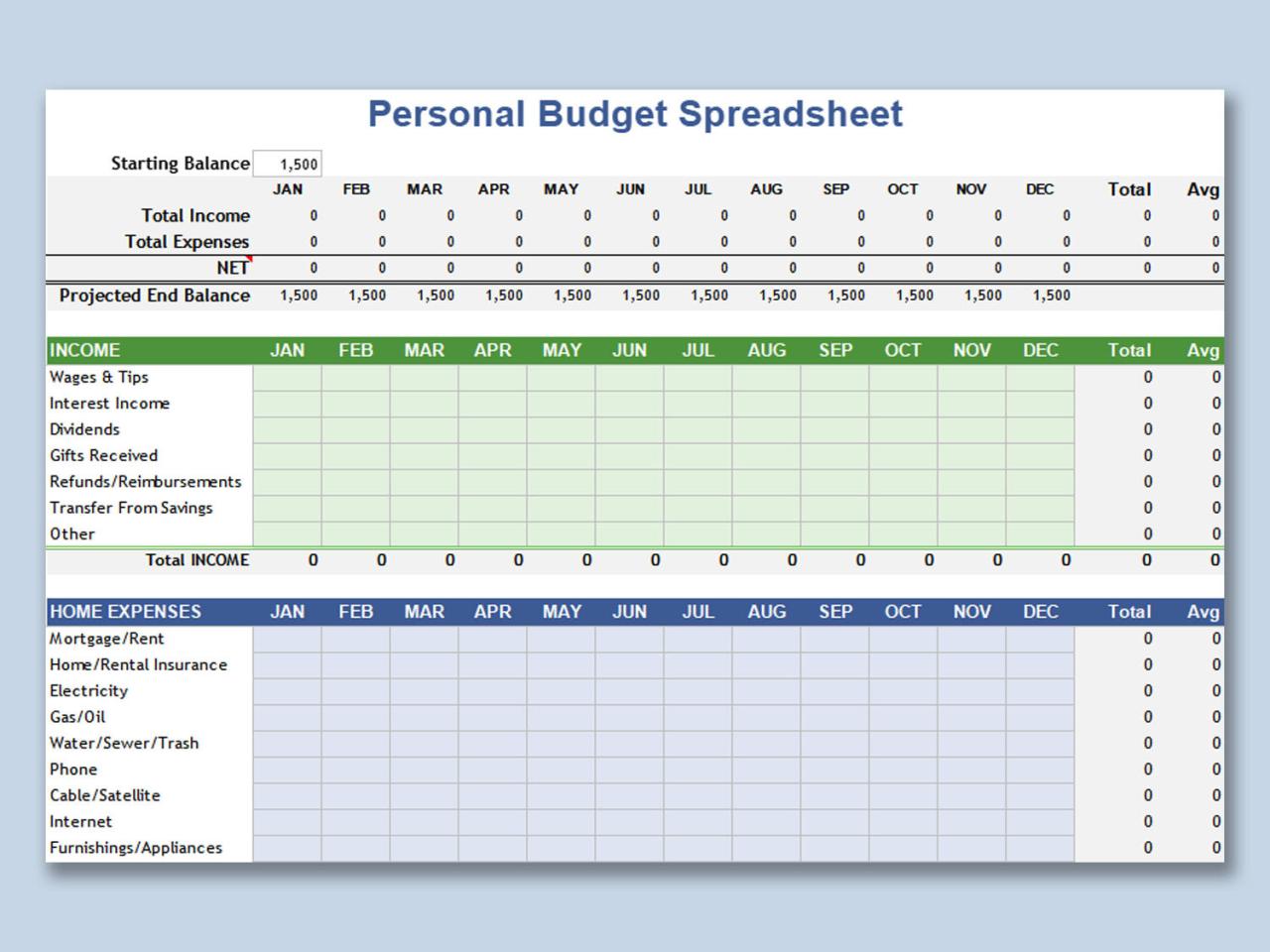

Setting up a budget within your chosen program is like building a financial fortress – a strong foundation is essential. Most programs offer intuitive interfaces, guiding you through the process. Generally, you’ll begin by inputting your monthly income, carefully categorizing every source (salary, freelance gigs, that surprisingly lucrative side hustle selling vintage rubber ducks – we don’t judge!). Then, you’ll allocate this income to various expense categories, such as housing, transportation, food, entertainment, and debt payments. Remember, accuracy is paramount here; overestimating income or underestimating expenses can lead to a budget collapse faster than a Jenga tower in a hurricane.

- Input Income: Enter all income sources meticulously. Don’t forget those sporadic bonuses or unexpected windfalls (Grandma’s unexpected inheritance, anyone?).

- Categorize Expenses: Most programs offer pre-defined categories, but feel free to customize them to reflect your unique spending habits. The more specific you are, the better you’ll understand your spending patterns. (Example: Instead of just “Food,” consider “Groceries,” “Eating Out,” and “Coffee”).

- Allocate Funds: Assign portions of your income to each expense category. This step requires careful planning and prioritization. Think of it as a financial tug-of-war – you want to balance your needs and wants without tipping the scales too far in one direction.

- Monitor and Adjust: Regularly review your budget, comparing your planned spending against actual spending. Life throws curveballs, so be prepared to adjust your budget as needed. Think of it as a living document, not a rigid set of rules.

Tracking Income and Expenses Accurately

Accurately tracking income and expenses is the bedrock of effective personal finance management. Think of it as being a financial detective – every penny has a story to tell, and you’re on the case! Most programs offer features like automatic transaction downloads from your bank accounts, simplifying the process. However, manual entry is sometimes necessary, especially for cash transactions or transactions not automatically synced.

Strategies for ensuring accuracy include:

- Regularly reconcile your accounts: Compare your program’s records to your bank statements. This helps identify any discrepancies and ensures everything is accounted for. Think of it as a financial audit, but much less intimidating (and hopefully, less expensive).

- Use descriptive transaction notes: Don’t just record “Groceries” – specify what you bought. “Groceries – Trader Joe’s – $75” is far more informative. This level of detail is like adding clues to your financial detective case.

- Categorize transactions consistently: Maintain a consistent categorization system throughout the month. Inconsistency can lead to skewed data and inaccurate budget projections. Think of it as maintaining order in your financial universe.

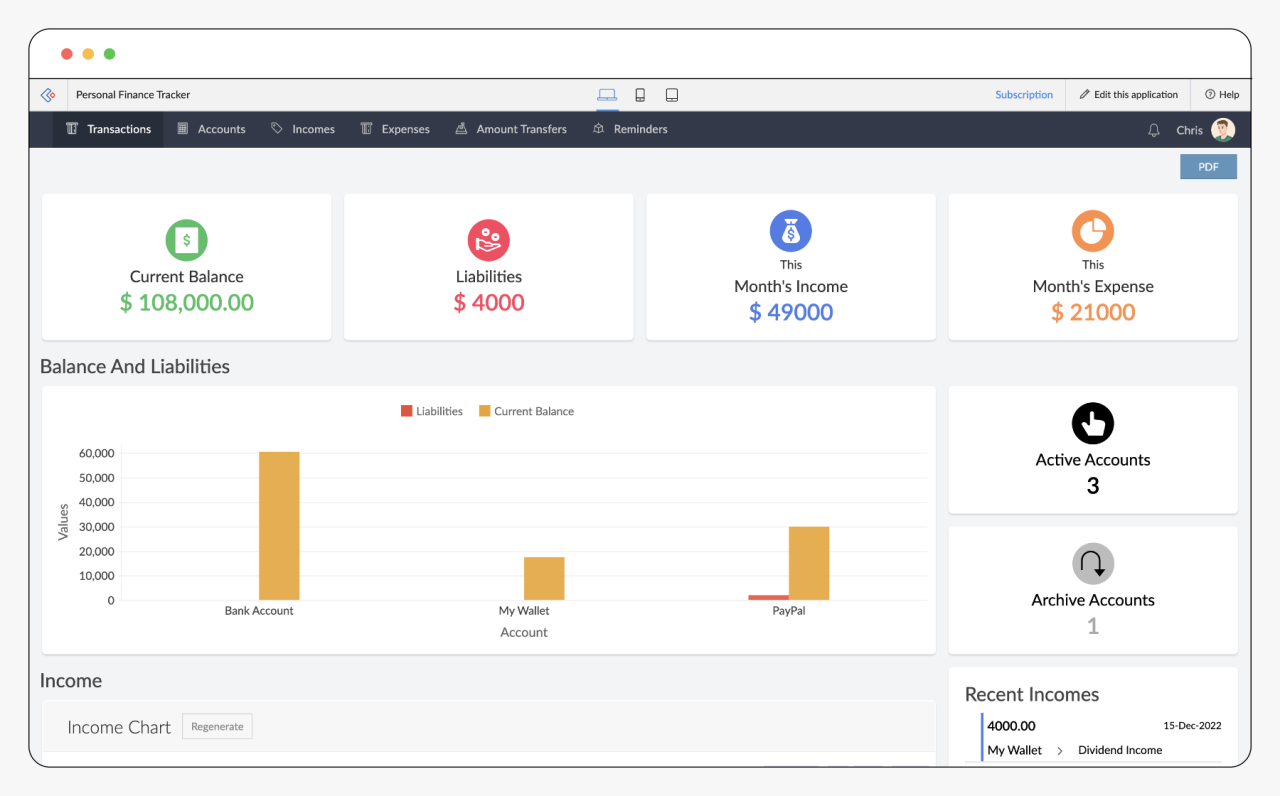

Creating and Monitoring Savings Goals

Setting savings goals within your program is like charting a course to your financial destination. Whether it’s a down payment on a house, a dream vacation, or early retirement, your program can help you stay on track. Most programs allow you to create custom savings goals, setting target amounts and deadlines. Some even offer progress tracking tools and visualizations (think fancy charts and graphs – because who doesn’t love a good chart?).

Effective strategies for monitoring savings goals include:

- Set SMART goals: Make your savings goals Specific, Measurable, Achievable, Relevant, and Time-bound. A vague goal like “save more money” is far less effective than “save $10,000 for a down payment in 18 months.”

- Regularly review progress: Check your progress towards your savings goals frequently. This keeps you motivated and allows you to adjust your savings strategy if necessary. Think of it as a pep talk, but for your bank account.

- Automate savings: Set up automatic transfers from your checking account to your savings account. This ensures you consistently save, even if you’re busy (or just easily distracted by shiny objects).

Data Security and Privacy

Let’s face it, your financial life is nobody’s business but your own. Unless, of course, you’re sharing it with a highly reputable personal finance program. But even then, caution is the name of the game. After all, your bank balance isn’t exactly something you want splashed across the internet like a particularly embarrassing vacation photo. This section explores the vital importance of safeguarding your sensitive financial information within these digital vaults.

Protecting your financial data is paramount when using personal finance programs. These programs often hold incredibly sensitive information, from your bank account details to your investment portfolios and even your spending habits (which, let’s be honest, can be quite revealing). A data breach could lead to identity theft, financial losses, and a whole lot of unnecessary stress – the kind that makes you want to hide under the covers with a giant tub of ice cream. So, choosing a program with robust security features isn’t just a good idea; it’s a necessity.

Evaluating Program Security Measures

Evaluating a personal finance program’s security involves more than just a cursory glance at their privacy policy (though, that’s a good start!). Look for evidence of robust encryption, both in transit and at rest. This means your data is scrambled when it’s being sent and stored, making it unreadable to prying eyes. Check for multi-factor authentication, which adds an extra layer of security beyond just a password. Think of it as a digital bouncer at the door of your financial data – only those with the right credentials (your password AND a code from your phone, for instance) can get in. Finally, research the company’s reputation and security track record. Have they experienced any data breaches in the past? A quick Google search can often reveal a lot.

Best Practices for Protecting Personal Financial Information

Protecting your financial information requires a multi-pronged approach. It’s like building a fortress – you need strong walls, a sturdy gate, and vigilant guards.

- Strong and Unique Passwords: Use a long, complex password that’s different from any other password you use. Password managers can be lifesavers here.

- Enable Two-Factor Authentication (2FA): This adds an extra layer of security, making it significantly harder for unauthorized individuals to access your account.

- Regular Software Updates: Keep your personal finance software and operating system up-to-date. These updates often include important security patches.

- Secure Your Devices: Use strong passwords and screen locks on all devices accessing your financial information. Consider using antivirus and anti-malware software.

- Beware of Phishing Scams: Never click on links or open attachments from unknown senders. Legitimate financial institutions will never ask for your password or other sensitive information via email.

- Monitor Your Accounts Regularly: Check your accounts frequently for any unauthorized activity. Catching suspicious transactions early can minimize potential losses.

- Choose Reputable Programs: Research the company behind the personal finance software. Look for evidence of strong security practices and a good reputation for data protection.

Program Limitations and Alternatives

Let’s face it, even the most sophisticated personal finance program can’t predict the next lottery win (unless it’s secretly working with the cosmic forces, which, let’s be honest, would be a *fantastic* feature). While these programs offer invaluable assistance, they’re not magic beans that instantly solve all your financial woes. Understanding their limitations and knowing when to explore alternative methods is crucial for maintaining a healthy financial life.

Program limitations often stem from the inherent simplicity of trying to capture the complexity of real-world finances. They excel at tracking transactions and projecting budgets, but less so at handling the nuanced aspects of investment strategies, tax implications, or the unpredictable nature of life events (like suddenly needing to fund a llama farm). This is where a balanced approach, considering both the strengths and weaknesses of different tools, becomes essential.

Limitations of Personal Finance Programs

Personal finance programs, while incredibly useful, are not without their limitations. They often lack the ability to provide personalized financial advice tailored to individual circumstances. For instance, a program might suggest a generic investment strategy, but it cannot account for specific risk tolerance, long-term goals, or the complexities of inheritance planning. Furthermore, data entry can be time-consuming, especially for individuals with numerous accounts or complex financial situations. Finally, the reliability of the program hinges on the accuracy of the data entered; garbage in, garbage out, as the saying goes. Incorrect information can lead to flawed projections and potentially detrimental financial decisions.

Alternative Methods for Managing Personal Finances

Sometimes, simpler is better. For individuals with relatively straightforward financial situations, a well-maintained spreadsheet might suffice. Imagine a beautifully organized spreadsheet, color-coded and meticulously updated – a financial masterpiece! This offers complete control and transparency, but requires significant self-discipline and a knack for formulas. On the other hand, engaging a financial advisor provides expert guidance, personalized strategies, and access to a wider range of financial products. This is particularly beneficial for individuals facing complex financial situations or those who prefer a hands-off approach to financial planning. However, the cost of a financial advisor needs to be factored into the equation.

Comparison of Personal Finance Programs, Spreadsheets, and Financial Advisors

| Method | Pros | Cons |

|---|---|---|

| Personal Finance Program | Automated tracking, budgeting tools, reporting features | Limited personalization, potential for data entry errors, subscription fees |

| Spreadsheet | Complete control, customizable, cost-effective | Requires significant time and effort, potential for errors, lacks automated features |

| Financial Advisor | Personalized advice, access to a wide range of financial products, expert guidance | High cost, potential for conflicts of interest |

The best approach often involves a combination of these methods. For example, a personal finance program could be used for daily transaction tracking, while a spreadsheet could be used for long-term financial projections, all under the guidance of a financial advisor for strategic decision-making. This hybrid approach leverages the strengths of each method while mitigating their individual weaknesses, leading to a more robust and comprehensive financial management strategy.