Best personal finance app? Ah, yes, the quest for the holy grail of budgeting! Finding the perfect app isn’t just about balancing your checkbook (though that’s a plus); it’s about finding a digital companion that understands your unique financial quirks. Whether you’re a meticulous saver, a spontaneous spender, or somewhere delightfully in between, the right app can transform your relationship with money from fraught to… well, less fraught. This exploration dives into the wild world of personal finance apps, examining the features, security, and user experience that make some shine brighter than others. Prepare for a financially enlightening adventure!

This guide navigates the often-bewildering landscape of personal finance apps. We’ll explore what makes an app truly “best” – a concept as subjective as your favorite ice cream flavor – by examining key features, security protocols, user interfaces, integration capabilities, pricing models, and illustrative examples of app functionality. We’ll even tackle those pesky privacy concerns, because your financial data deserves the same level of protection as your prized collection of rubber ducks.

Defining “Best”: Best Personal Finance App

Finding the *best* personal finance app is a bit like finding the perfect pair of shoes – it depends entirely on the foot (or, in this case, the financial situation) doing the wearing. There’s no single, universally agreed-upon “best” app, because our financial lives are as diverse and quirky as we are. What works wonders for a meticulous budgeter might feel clunky and restrictive for someone who prefers a more hands-off approach.

Individual preferences for personal finance apps are shaped by a multitude of factors. Consider your comfort level with technology, the complexity of your financial life (multiple accounts, investments, debts), your preferred method of tracking expenses (manual entry, bank connections, etc.), and even your personality type. Are you a data-driven individual who thrives on detailed charts and graphs? Or do you prefer a simpler, more intuitive interface that gets the job done without overwhelming you with information? These seemingly minor details significantly impact the app’s perceived “bestness.”

User Profiles and App Preferences, Best personal finance app

The following table illustrates how diverse financial needs and goals lead to different app priorities. Imagine these profiles as representing a spectrum of users, each with unique requirements that a suitable app must address.

| User Profile | Primary Financial Goal | App Priorities | Example App Feature (Hypothetical) |

|---|---|---|---|

| The Frugal Freshman | Building an emergency fund, minimizing debt | Simple budgeting tools, clear expense tracking, debt management features | A “Savings Challenge” feature gamifying the saving process with rewards and milestones. |

| The Aspiring Investor | Growing investments, long-term financial planning | Portfolio tracking, investment analysis tools, integration with brokerage accounts | Automated portfolio rebalancing suggestions based on risk tolerance and market trends. |

| The Business Owner | Managing business finances, tracking income and expenses | Invoicing capabilities, expense reporting features, tax preparation integration | Automated categorization of business expenses based on s in transaction descriptions. |

| The Debt Warrior | Paying off high-interest debt, improving credit score | Debt snowball/avalanche calculators, credit score monitoring, budgeting tools focused on debt reduction | Personalized debt repayment plans adjusting to unexpected income fluctuations. |

| The Family Planner | Managing household finances, planning for future expenses (education, retirement) | Shared account features, budgeting tools for multiple income streams, goal-setting tools | Automated allocation of funds to various savings goals based on predefined percentages. |

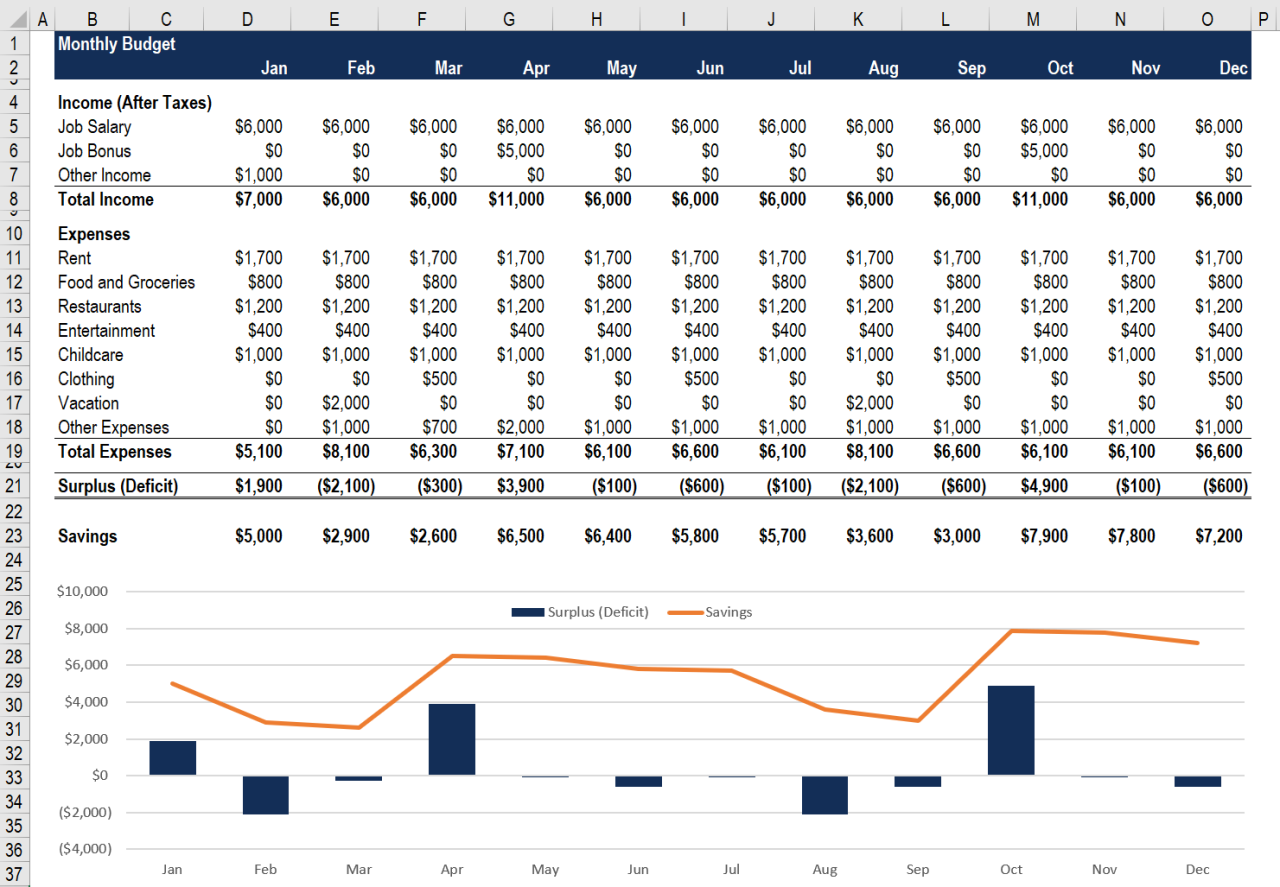

Different apps cater to these diverse needs in various ways. For example, a simple budgeting app might excel at basic expense tracking, while a more comprehensive app might offer advanced features like investment portfolio management and tax planning tools. The “best” app is the one that best aligns with your specific financial goals and preferences. It’s all about finding the perfect fit.

Security and Privacy Considerations

Protecting your financial data is paramount, and frankly, more exciting than balancing your checkbook (we’re kidding…mostly). A truly “best” personal finance app understands this and employs robust security measures to safeguard your sensitive information from prying eyes – both digital and otherwise. Think of it as a financial Fort Knox, but with a much nicer interface.

Data encryption and security protocols are the unsung heroes of secure personal finance apps. These aren’t just buzzwords; they’re the technological guardians preventing unauthorized access to your financial details. Without them, your meticulously tracked budget could become a digital buffet for cyber-criminals. This section will delve into the specifics of how these protections work and the types of data involved.

Data Encryption and Security Protocols

Strong encryption, like the unbreakable code of a particularly clever spy novel, is crucial. This involves scrambling your data into an unreadable format, rendering it useless to anyone without the decryption key. Think of it as wrapping your financial information in layers upon layers of impenetrable wrapping paper, only to be unwrapped by you, and only you, with your unique digital key. Furthermore, secure apps employ multi-factor authentication (MFA), adding an extra layer of protection beyond just a password. This could involve a one-time code sent to your phone or email, making unauthorized access significantly more difficult, even if your password is somehow compromised. Robust security protocols also include regular security audits and penetration testing to proactively identify and address vulnerabilities before they can be exploited. Imagine it as a team of highly trained financial ninjas constantly patrolling your digital fortress.

Data Collected and Privacy Policies

Personal finance apps, naturally, collect data to function. This typically includes transaction details (amounts, dates, merchants), account balances, budgeting information, and potentially even investment details. A responsible app will clearly Artikel what data is collected, why it’s collected, and how it’s used in its privacy policy. This isn’t some legal mumbo-jumbo designed to confuse; it’s a transparent commitment to user privacy. A good privacy policy will also explain how the app protects your data from unauthorized access and what measures are in place to prevent data breaches. Think of it as a contract that protects your financial privacy – a contract you should absolutely read!

Hypothetical Privacy Policy Excerpt for a Secure Personal Finance App

Our commitment to your privacy is absolute. We employ bank-level encryption (AES-256) to protect all your financial data both in transit and at rest. Your data is never sold to third parties. We use your data solely to provide you with the best possible personal finance management experience and to improve our app’s functionality. We comply with all relevant data protection regulations, including [insert relevant regulations, e.g., GDPR, CCPA]. We implement strict access controls, limiting access to your data to authorized personnel only. We conduct regular security audits and penetration testing to identify and address vulnerabilities promptly. You have the right to access, correct, or delete your data at any time. We will promptly notify you in the unlikely event of a data breach. We are committed to transparency and will readily respond to any questions you have regarding our privacy practices.

Integration with Other Financial Services

Ah, the holy grail of personal finance apps: seamless integration. Imagine a world where your bank balance, credit card spending, and investment portfolio all harmonize in one beautifully orchestrated financial symphony. No more frantic toggling between multiple apps, no more spreadsheets resembling a Jackson Pollock painting – just a clear, concise picture of your financial well-being. This, my friends, is the promise of integrated personal finance apps.

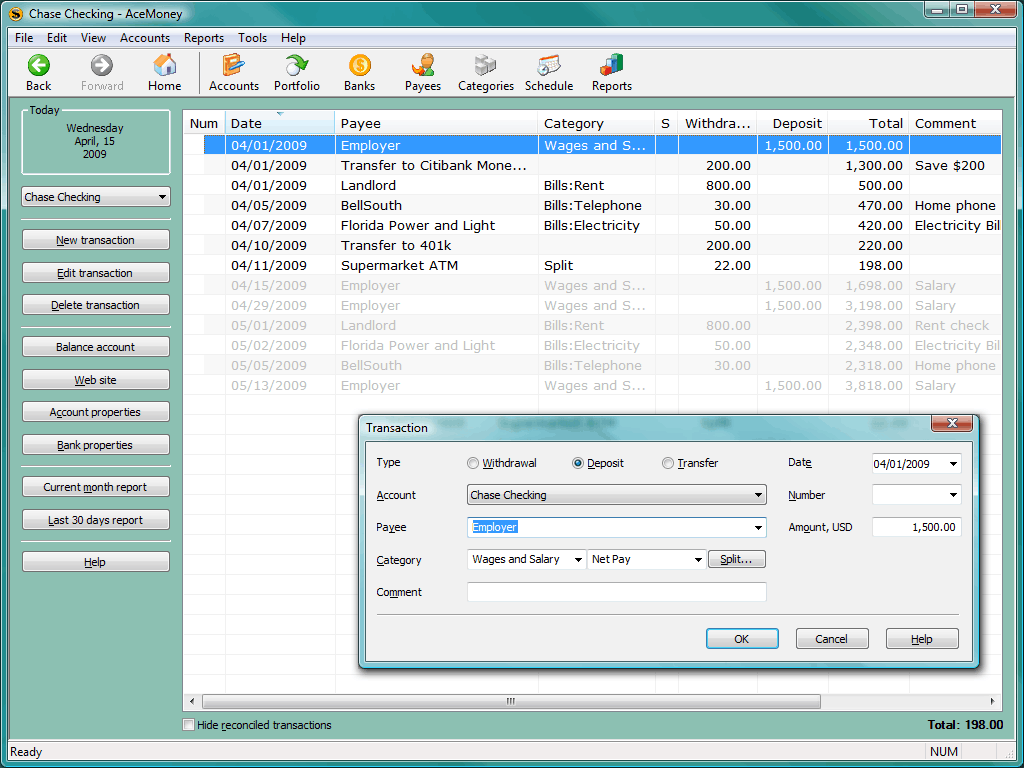

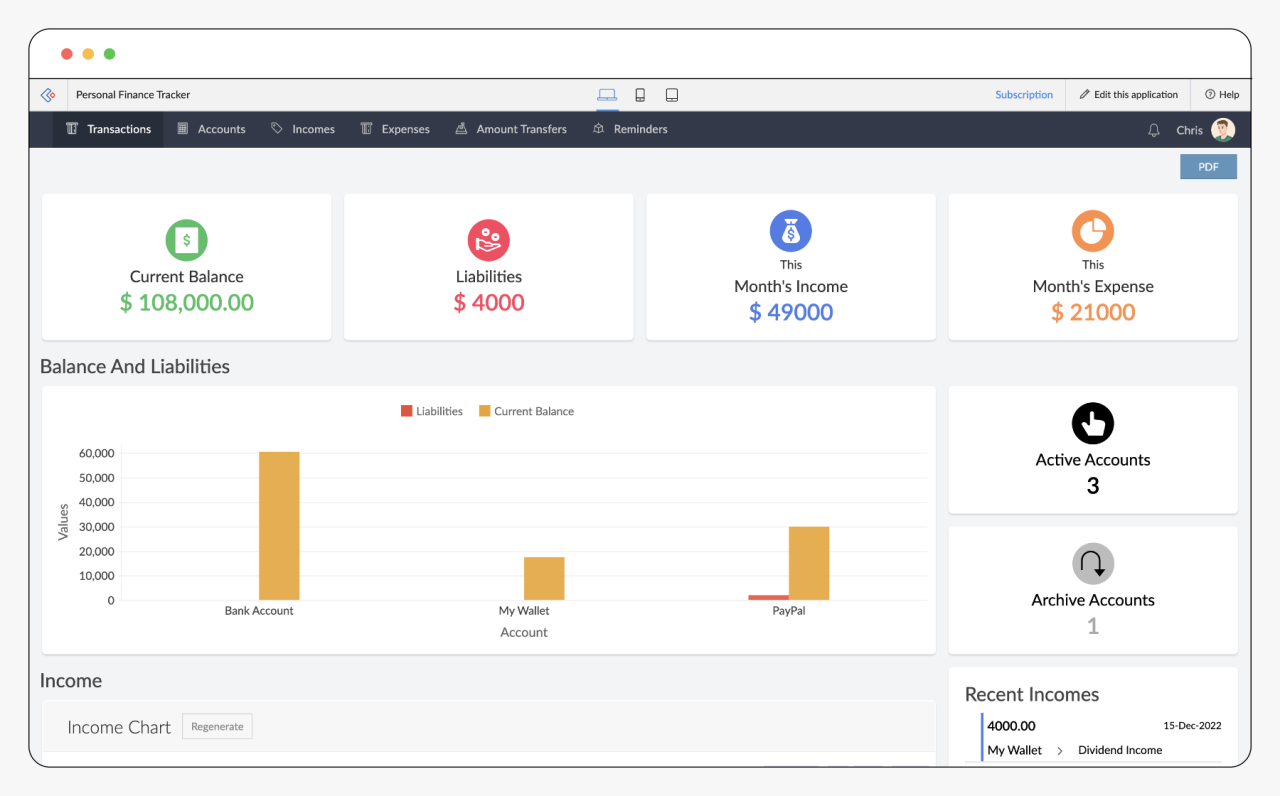

Seamless integration with your various financial accounts simplifies your life considerably. It automates data entry, eliminating the tedious manual input that can lead to errors and frustration. Accurate, up-to-the-minute data allows for more informed financial decisions, leading to better budgeting, smarter investing, and a reduced risk of overspending (or, let’s be honest, accidentally buying that limited-edition avocado toast maker you *definitely* don’t need). This streamlined approach saves you valuable time and mental energy, allowing you to focus on the more important things in life, like deciding which flavor of artisanal ice cream to indulge in.

Comparison of Integration Capabilities Across Three Leading Apps

Let’s examine the integration prowess of three hypothetical leading personal finance apps: “MoneyMind,” “FinanceFlow,” and “BudgetBuddy.” Each app offers a unique approach to connecting with your financial ecosystem, showcasing the diverse landscape of integration capabilities.

| App Name | Bank Accounts | Credit Cards | Investment Platforms |

|---|---|---|---|

| MoneyMind | Direct connection via Plaid; supports over 15,000 banks. Manual import also available via CSV. | Automatic transaction import via direct connection; supports most major credit card issuers. | Integrates with brokerage accounts from Fidelity, Schwab, and Vanguard; supports manual import of transactions from other platforms. |

| FinanceFlow | Screen scraping technology; supports a wide range of banks but may have compatibility issues with smaller institutions. Manual import also an option. | Supports automatic transaction import for most major credit cards, though sometimes requires manual account verification. | Limited integration; primarily focuses on brokerage accounts from major institutions. Relies heavily on manual data entry for other investment platforms. |

| BudgetBuddy | Relies primarily on manual data entry; offers limited direct connection options. | Manual data entry is the primary method of integration. | No direct integration; users must manually input investment data. |