Top free personal finance software unlock your financial potential – Top free personal finance software: unlock your financial potential! Forget the Scrooge McDuck money bin – we’re talking about digitally organized wealth, my friends. This isn’t your grandpappy’s ledger book; we’re diving into the exciting world of free software designed to tame your finances and help you finally understand where your money goes (and, more importantly, *where* it should go). Prepare for a journey into budgeting bliss, investment enlightenment, and debt-crushing strategies, all without breaking the bank (ironically).

This guide explores the best free personal finance software available, comparing their features, strengths, and weaknesses. We’ll cover everything from basic budgeting tools to sophisticated investment tracking, offering practical advice and actionable steps to help you take control of your financial future. We’ll even tackle those tricky security and privacy concerns – because let’s face it, nobody wants their financial secrets exposed to the digital equivalent of a nosy neighbor.

Budgeting and Expense Tracking Capabilities: Top Free Personal Finance Software Unlock Your Financial Potential

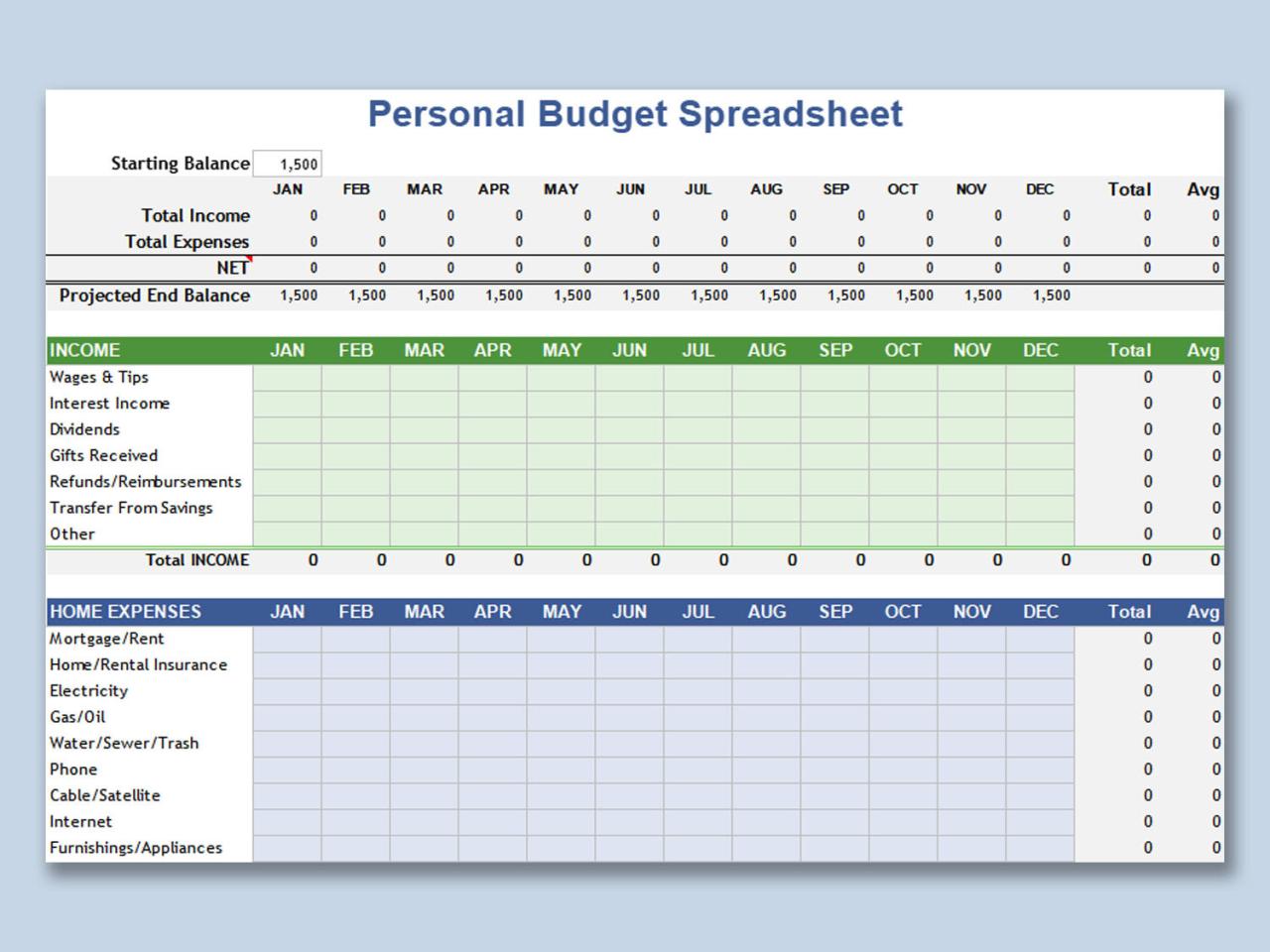

Ah, budgeting. The word itself can conjure images of tedious spreadsheets and soul-crushing self-denial. But fear not, dear reader! With the right free personal finance software, budgeting can transform from a chore into a surprisingly satisfying journey towards financial freedom (and maybe even a little bit of fun!). We’re talking about taking control of your money, not letting it control you. Think of it as a financial makeover, but instead of a new haircut, you get a new, healthier relationship with your bank account.

The importance of budgeting in personal finance is paramount. It’s the roadmap to your financial destination, guiding you away from the treacherous cliffs of overspending and towards the sunny shores of financial stability. Without a budget, you’re essentially navigating life’s financial waters blindfolded, hoping for the best while bracing for the worst. A budget allows you to see exactly where your money is going, identify areas for improvement, and make informed decisions about your spending habits. It’s like having a financial GPS, except instead of directions to the nearest Starbucks, it guides you to your financial goals.

Expense Tracking Methods Employed by Software

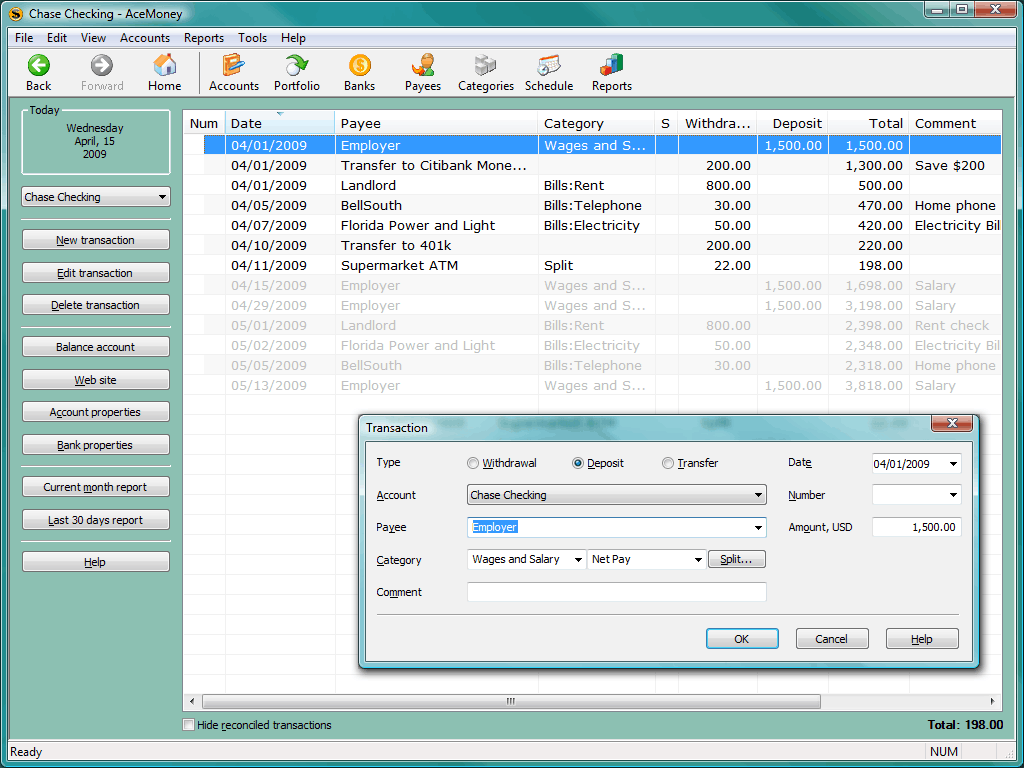

Various software programs utilize different methods to track expenses. Many employ a simple, intuitive interface where users manually input their transactions. This might involve categorizing expenses (e.g., groceries, entertainment, rent) and assigning them to specific accounts. Some more advanced programs offer features like automatic transaction import from linked bank accounts, reducing manual data entry significantly. Imagine the time saved! You could be using that time to, say, enjoy a well-deserved cup of coffee (budget permitting, of course). Others integrate with credit card companies to provide a seamless and automated expense tracking experience. The best software will cater to your preferred method of tracking and adapt to your personal needs and level of tech-savviness.

Budgeting Methods Supported by Free Software

Free personal finance software often supports a variety of budgeting methods. Let’s explore a couple of popular choices:

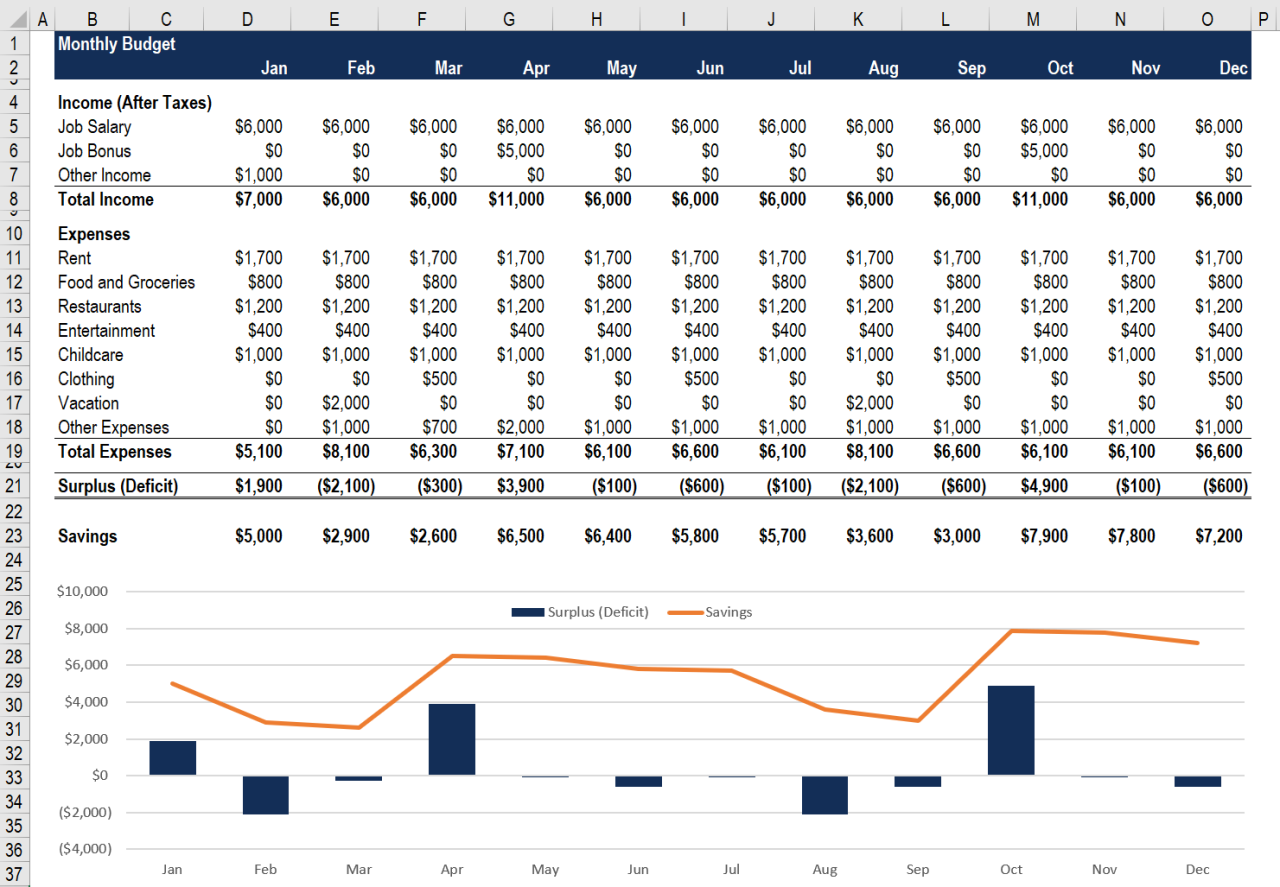

The 50/30/20 rule is a simple yet effective approach. It suggests allocating 50% of your after-tax income to needs (housing, food, transportation), 30% to wants (entertainment, dining out, hobbies – the fun stuff!), and 20% to savings and debt repayment. It’s a great starting point for those new to budgeting, offering a clear framework for managing finances. Think of it as a financial training wheel; it helps you stay balanced until you’re ready to ride solo.

Zero-based budgeting, on the other hand, takes a more meticulous approach. Every dollar is assigned a specific purpose. This means you need to meticulously account for every penny of your income, ensuring that all your expenses are covered, leaving a zero balance. While initially more demanding, this method provides a very granular understanding of your finances, making it easier to spot unnecessary spending and adjust your budget accordingly. It’s like a financial audit, but you get to do it yourself and, hopefully, avoid the hefty fees.

Creating a Monthly Budget Using Free Software: A Step-by-Step Guide

Let’s assume you’ve chosen a free personal finance software (many excellent options are available!). Here’s a general guide, adaptable to most programs:

1. Account Setup: Create an account and link your bank accounts and credit cards (if the software supports this). This enables automatic transaction importing, saving you valuable time.

2. Income Entry: Input your monthly income from all sources (salary, side hustles, investments). Be precise! Even small amounts matter in the grand scheme of your financial picture.

3. Expense Categorization: Categorize your expenses using the software’s pre-defined categories or create your own. Consistency is key here; it’s important to categorize expenses similarly each month for accurate tracking.

4. Budget Allocation: Allocate your income across your various expense categories based on your chosen budgeting method (50/30/20, zero-based, or a customized approach).

5. Regular Monitoring: Regularly review your budget to track your progress and identify areas where you might be overspending. Regular monitoring will give you a sense of control and keep you on track. Think of it as a friendly financial check-up.

Remember, the key to successful budgeting isn’t about strict deprivation; it’s about making conscious choices about how you spend your money so you can achieve your financial goals. And with the right free software, that process can be surprisingly painless (and maybe even a little fun!).

Investing and Portfolio Management Features

Free personal finance software offers a surprisingly robust, albeit sometimes quirky, entry point into the world of investment tracking. While they might not replace the sophisticated algorithms of professional-grade platforms, these tools can be invaluable for beginners or those managing simpler portfolios, providing a user-friendly way to monitor assets and, dare we say, maybe even inspire some healthy financial habits (we’re cautiously optimistic here). Think of it as your friendly neighborhood financial sidekick, ready to help you keep tabs on your investments without breaking the bank.

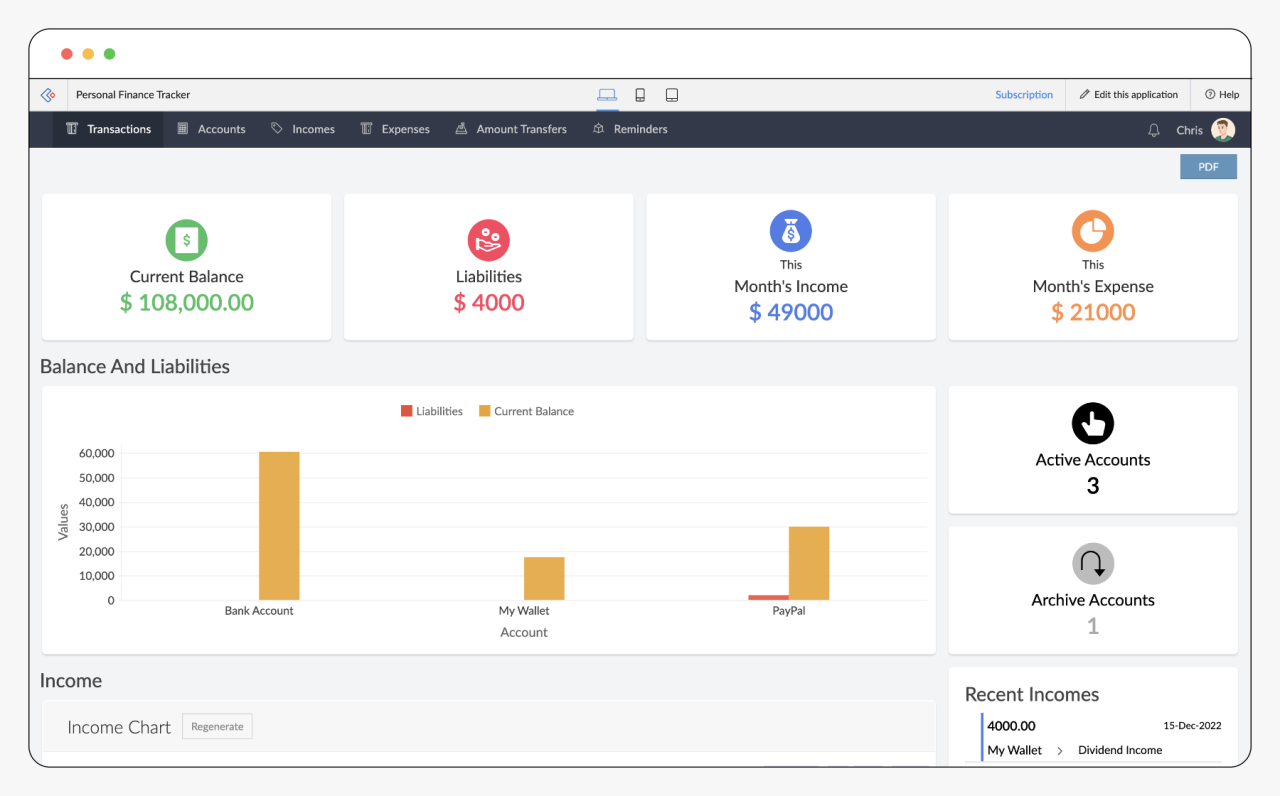

Free software’s role in managing investments primarily centers on organization and monitoring. It allows individuals to input their holdings, track their performance over time, and generate basic reports, all without the hefty price tag of premium services. This can be particularly helpful for visual learners who appreciate seeing their investments laid out in charts and graphs, offering a clearer picture of their overall financial health than a simple spreadsheet ever could. The ability to easily see your gains (or losses, let’s be honest, those happen too) can be a powerful motivator for better financial decision-making.

Limitations of Free Investment Software

Free software, while convenient, inherently has limitations when dealing with complex investment strategies. For example, most lack advanced features like sophisticated tax-loss harvesting algorithms, automated portfolio rebalancing based on complex rules, or real-time market data feeds with fractional-share precision. These features are often reserved for paid platforms catering to more experienced investors with more nuanced needs. Trying to manage a complex options trading strategy or a highly diversified portfolio across numerous asset classes with free software would likely be akin to navigating a minefield blindfolded – potentially thrilling, but definitely risky. In short, free software excels at basic tracking, but falls short when dealing with the intricacies of advanced investment strategies.

Comparison of Investment Tracking Features

Let’s consider two hypothetical examples of free personal finance software, “BudgetBuddy Pro Max” (which is entirely fictional, by the way) and “MoneyWise 2000” (also fictional, for legal reasons). BudgetBuddy Pro Max boasts a sleek, modern interface with interactive charts showing portfolio performance over various timeframes. It allows for the categorization of assets (stocks, bonds, ETFs, etc.) and provides basic performance metrics like total return and average annual growth. MoneyWise 2000, on the other hand, takes a more spreadsheet-like approach, offering detailed input fields for individual securities and a robust reporting engine capable of generating customized reports. However, its user interface is, shall we say, less visually appealing. Ultimately, the best choice depends on individual preferences: BudgetBuddy Pro Max for visual learners, and MoneyWise 2000 for those who prefer detailed, data-driven analysis.

Potential Risks of Using Free Software for Investment Management

It’s crucial to acknowledge the inherent risks associated with relying solely on free investment management software. One key concern is data security. Free services might not offer the same level of encryption and data protection as paid platforms, leaving your sensitive financial information potentially vulnerable. Another risk is the potential for inaccuracies or bugs in the software itself, leading to incorrect calculations or misleading reports. Remember that you, the user, are ultimately responsible for the accuracy of your data input and interpretation of the results. Finally, the limitations in features mentioned earlier could lead to suboptimal investment decisions if you attempt to stretch the software beyond its capabilities. Using free software for investment management is like using a basic calculator for advanced calculus – you might get some answers, but you’ll likely miss some crucial details.

Debt Management Tools and Strategies

Conquering debt can feel like scaling Mount Everest in flip-flops, but fear not, intrepid financial adventurer! Free personal finance software can be your trusty Sherpa, guiding you to the summit of financial freedom. These digital tools provide the structure and insights needed to tackle even the most daunting debt challenges. They’re not magic wands (sadly, no instant debt disappearance!), but they are powerful allies in your debt-reduction journey.

Free software offers a range of features designed to help you manage and reduce your debt effectively. Imagine having a personal financial assistant that meticulously tracks your payments, analyzes your progress, and even suggests strategies for faster debt elimination. This isn’t a fantasy; it’s the reality offered by many readily available, free applications. They empower you to take control of your finances and craft a personalized debt repayment plan, transforming a stressful situation into a manageable, and even potentially enjoyable, challenge.

Debt Reduction Strategies

Effective debt reduction strategies aren’t about blind luck; they’re about informed choices and consistent action. Two popular approaches are the debt snowball and debt avalanche methods. Both methods involve prioritizing certain debts for faster repayment, but they differ in their approach.

Debt Snowball Method

The debt snowball method prioritizes paying off the smallest debts first, regardless of interest rates. This approach focuses on building momentum and psychological wins. The satisfaction of quickly eliminating smaller debts motivates continued effort and fosters a sense of accomplishment, fueling perseverance towards larger debts. Imagine the exhilaration of crossing off those smaller debts – a mini-celebration with every victory! This psychological boost can be invaluable in maintaining long-term commitment to your debt repayment plan. Think of it as a series of smaller, achievable goals leading to the ultimate prize: a debt-free life.

Debt Avalanche Method

In contrast, the debt avalanche method prioritizes debts with the highest interest rates. While this approach might not offer the same immediate psychological gratification as the debt snowball method, it ultimately saves money on interest in the long run. By focusing on the most expensive debts first, you minimize the total interest paid over the life of your debts, leading to significant savings. This is a mathematically sound approach, prioritizing efficiency and long-term financial gain.

Tracking Debt Payments and Creating a Repayment Plan

Many free personal finance software programs allow you to input your debt information (creditor, balance, interest rate, minimum payment). The software then calculates the total interest paid and the time it will take to repay your debts under various scenarios. You can then experiment with different payment amounts to see how this affects your repayment timeline and overall interest paid. This allows for a dynamic approach, enabling you to adjust your strategy based on your financial circumstances and goals. The software becomes your personal financial laboratory, allowing you to test different approaches before committing to a specific plan.

Visual Representation of Debt Repayment Strategies, Top free personal finance software unlock your financial potential

Imagine two bar graphs representing debt repayment. One graph (Debt Snowball) shows several short bars representing smaller debts, quickly shrinking and disappearing one by one. The longer bars representing larger debts shrink more slowly, but the visual momentum is clear. The second graph (Debt Avalanche) shows a different picture. The tallest bars (highest interest rate debts) decrease rapidly, though the overall visual progress might appear slower initially. However, the total area under the graph (representing total debt) decreases faster in the long run due to the significant reduction in interest payments. This visual comparison highlights the trade-off between psychological momentum and long-term financial efficiency.

Unlocking Financial Potential Through Software

Harnessing the power of free personal finance software isn’t just about balancing your checkbook (though that’s a definite plus!). It’s about gaining a crystal-clear view of your financial landscape, empowering you to make smarter decisions and, dare we say it, actually *enjoy* the process. Think of it as your very own financial Sherpa, guiding you towards the summit of financial freedom – without the altitude sickness.

Free personal finance software offers a surprisingly potent cocktail of features designed to transform your financial life from a chaotic mess into a well-oiled, money-making machine. These tools provide the structure and insights necessary to move beyond simply tracking income and expenses; they allow you to actively strategize, plan, and achieve your financial aspirations. It’s like having a personal financial advisor who works for free (and doesn’t judge your occasional impulse buys…much).

Improved Financial Well-being Through Software Use

Utilizing free personal finance software directly contributes to improved financial well-being by providing a comprehensive overview of your financial situation. This clarity allows for informed decision-making, reducing financial stress and promoting better money management habits. For example, a user consistently tracking their spending might discover they’re overspending on coffee – a revelation leading to a simple but impactful change. The software doesn’t just show you the problem; it empowers you to solve it. This improved awareness translates into a reduction in financial anxiety and a greater sense of control over one’s finances. This control is the key to unlocking a more peaceful and prosperous future.

Leveraging Software to Achieve Financial Goals

Free personal finance software facilitates goal achievement through various features. Budgeting tools allow users to allocate funds effectively towards specific goals, such as saving for a down payment or paying off debt. Investing features offer insights into portfolio performance and diversification strategies, helping users make informed investment decisions. Debt management tools provide structured plans to tackle high-interest debts, accelerating the path to financial freedom. For instance, a user aiming to buy a house can utilize the software to track their savings progress, visualize their target date, and adjust their budget accordingly. The software provides the visual roadmap and the tools to stay on track.

Benefits of Tracking Financial Progress and Setting Realistic Goals

Tracking financial progress is crucial for maintaining motivation and identifying areas needing improvement. Setting realistic financial goals, broken down into smaller, achievable milestones, prevents discouragement and promotes a sense of accomplishment. For example, instead of aiming for a massive debt payoff in one year, a more realistic approach might involve setting quarterly goals, celebrating each milestone reached. This strategy provides consistent positive reinforcement, increasing the likelihood of long-term success. The software provides the tools to visualize progress, reinforcing positive behaviors and offering encouragement along the way.

Actionable Steps to Maximize Software Benefits

The key to unlocking the full potential of free personal finance software lies in proactive engagement.

Below are actionable steps users can take to maximize the benefits:

- Complete and Accurate Data Entry: Regular and accurate data entry is paramount. Garbage in, garbage out, as they say. The more complete your data, the more accurate and insightful your financial picture will be.

- Regularly Review Reports and Analytics: Don’t just input data; actively review the reports and analytics generated by the software. These insights will highlight areas for improvement and inform your financial decisions.

- Set Realistic and Measurable Goals: Set SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound). This approach ensures your goals are well-defined and trackable.

- Utilize All Available Features: Explore all the features offered by your chosen software. Many offer budgeting tools, investment tracking, debt management features, and more. Take advantage of them all!

- Regularly Adjust Your Plan: Life happens. Be prepared to adjust your financial plan as needed. The software provides the flexibility to adapt to changing circumstances.