r Personal Finance: Navigating the sometimes-bewildering world of personal finance doesn’t have to feel like scaling Mount Everest in flip-flops. This guide provides a humorous yet practical approach to budgeting, saving, investing, and debt management, transforming the often-dreaded topic into an engaging journey towards financial freedom. We’ll tackle everything from crafting a killer budget to outsmarting those sneaky credit card interest rates, all while keeping things light and informative.

Whether you’re a fresh-faced graduate entering the workforce or a seasoned professional looking to fine-tune your financial strategy, this guide offers actionable steps and insightful tips to help you build a solid financial foundation. We’ll explore various saving and investing strategies, discuss effective debt reduction techniques, and even delve into the sometimes-mysterious world of retirement planning. Get ready to ditch the financial anxieties and embrace a brighter, more financially secure future!

Debt Management and Reduction: R Personal Finance

Ah, debt. That delightful little albatross around your financial neck. Let’s not beat around the bush; it’s a pain, but conquering it is entirely possible, even enjoyable (in a masochistic, spreadsheet-loving kind of way). This section will equip you with the tools to not only survive but thrive in the face of your outstanding obligations. We’ll tackle creating a debt repayment plan, negotiating lower interest rates, and avoiding those pesky pitfalls that can send you spiraling back into the red. Buckle up, it’s going to be a wild ride!

Effective debt management requires a strategic approach, focusing on minimizing interest payments and accelerating repayment. This involves careful planning, disciplined budgeting, and potentially some skillful negotiation.

Creating a Debt Repayment Plan, R personal finance

Before you even think about tackling your debt, you need a battle plan. This isn’t some haphazard approach; it’s a carefully crafted strategy for financial victory. The following steps will guide you through the process of creating a comprehensive debt repayment plan, prioritizing high-interest debts to minimize overall interest paid.

- List all your debts: Include the creditor, the balance, the interest rate (APR), and the minimum payment amount. This detailed inventory is your first step towards financial clarity.

- Prioritize your debts: Employ the avalanche method (focus on the highest interest rate debt first) or the snowball method (focus on the smallest debt first for psychological motivation). Both are valid; choose the one that best suits your personality and financial situation.

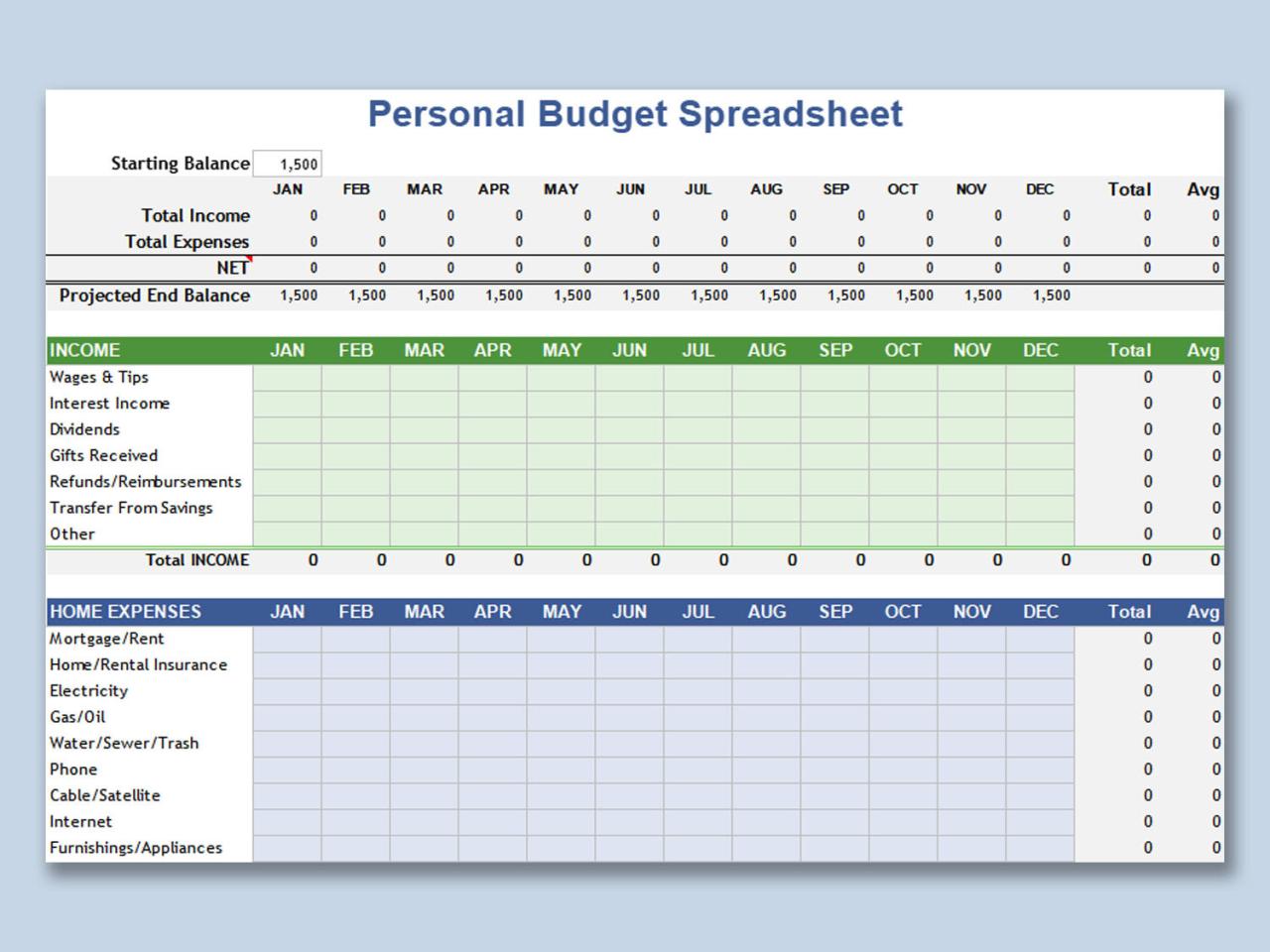

- Create a budget: Track your income and expenses meticulously. Identify areas where you can cut back to free up extra funds for debt repayment. This isn’t about deprivation; it’s about strategic allocation of resources.

- Allocate extra funds: Once you have a clear budget, allocate as much extra money as possible towards your highest-priority debt. Every extra dollar counts!

- Make consistent payments: Regularity is key. Set up automatic payments to ensure you never miss a deadline and avoid late fees, which can quickly derail your progress.

- Celebrate milestones: Acknowledge your progress along the way. Paying off a debt, no matter how small, is a significant accomplishment. Reward yourself appropriately (without resorting to further debt!).

Negotiating Lower Interest Rates

Negotiating lower interest rates can significantly reduce the overall cost of your debt. It requires confidence, preparation, and a touch of charm. Remember, the worst they can say is no!

Effective negotiation often involves demonstrating your commitment to repayment and highlighting your positive financial history (where applicable). For example, you might mention consistent on-time payments in the past. You can also inquire about balance transfer options or debt consolidation programs which could offer lower interest rates.

Example: Imagine you’ve been diligently paying your credit card bill for years. Call your credit card company and politely explain your situation. Express your desire to continue being a loyal customer but inquire about a lower interest rate given your consistent payment history. Many companies are willing to work with responsible customers.

Avoiding Debt Management Pitfalls

Navigating the world of debt requires vigilance. Several common pitfalls can easily derail even the most well-intentioned plans. Let’s address them head-on.

- Impulse Purchases: The siren song of instant gratification is a dangerous one. Avoid making unnecessary purchases, especially on credit. Before buying anything, ask yourself if it’s truly necessary and if you can afford it without adding to your debt.

- Over-Reliance on Credit Cards: Credit cards are convenient, but they can quickly become a financial millstone if not managed responsibly. Avoid maxing out your cards and always strive to pay off your balance in full each month. If you can’t, consider cutting up your cards to break the cycle of overspending.

- Ignoring Your Debt: Pretending your debt doesn’t exist won’t make it disappear. Facing your financial realities and actively working towards a solution is crucial. Ignoring debt can lead to escalating interest charges, collection calls, and even legal action.