Best personal finance software isn’t just about balancing your checkbook; it’s about taking control of your financial future. From tracking every latte to meticulously managing investments, the right software can transform your relationship with money. This guide dives deep into the world of personal finance software, exploring features, pricing models, and user needs to help you find the perfect fit, regardless of whether you’re a penny-pinching student or a high-flying entrepreneur. We’ll navigate the sometimes-murky waters of budgeting, investing, and debt management, emerging with a clear understanding of how to harness technology for your financial well-being.

Choosing the right software can feel like choosing a life partner – a long-term commitment requiring careful consideration. This guide provides a structured approach, allowing you to evaluate different software options based on your specific financial goals and tech proficiency. We’ll explore everything from user-friendly interfaces to robust security features, ensuring you make an informed decision that empowers you to take charge of your financial destiny. Forget spreadsheets and sticky notes – let’s find the software that will help you conquer your financial goals.

Defining “Best” in Personal Finance Software

Finding the “best” personal finance software isn’t about discovering a mythical unicorn; it’s about finding the software that best fits your unique financial circumstances and personality. Think of it like choosing a pair of shoes – you wouldn’t wear hiking boots to a gala, would you? Similarly, the ideal software for a student will differ greatly from the needs of a family with multiple income streams and investments.

Defining “best” hinges on a confluence of factors, primarily your individual needs, your budget (because let’s be honest, free is often best!), and your comfort level with technology. Someone tech-savvy might appreciate a highly customizable program with advanced features, while someone less inclined towards tech might prefer a simpler, more intuitive interface. The ideal software should be a helpful assistant, not a source of frustration.

Essential Features Based on User Type

The essential features of a good personal finance program vary depending on the user’s situation. A one-size-fits-all approach is as sensible as wearing mismatched socks. Below, we categorize key features according to different user types.

Students might prioritize features that help them track expenses and budget effectively for tuition, books, and living expenses. Freelancers, on the other hand, require robust invoicing capabilities and tax reporting tools. Families may need features to manage shared accounts, track household expenses, and plan for long-term financial goals like college funds or retirement.

- Students: Expense tracking, budgeting tools (e.g., 50/30/20 rule implementation), simple reporting, goal setting (e.g., saving for tuition).

- Freelancers: Income and expense tracking, invoicing, expense categorization for tax purposes, tax report generation, time tracking (optional but helpful).

- Families: Shared account management, multiple budget categories, bill tracking, investment tracking, goal setting (e.g., retirement planning, college savings).

User Scenarios and Software Feature Solutions, Best personal finance software

Let’s consider some real-world examples. Imagine a young professional saving for a down payment on a house. The ideal software would allow them to set a savings goal, track their progress, and automatically categorize their transactions to easily see where their money is going. For a family managing multiple accounts and investments, features like shared access, investment tracking, and comprehensive reporting would be crucial. A freelancer needing to manage irregular income would benefit from robust invoicing tools and the ability to easily track expenses for tax purposes.

Pricing Models Comparison

Choosing the right pricing model is as crucial as selecting the right features. Here’s a comparison of three common models:

| Feature Set | Price | Target User |

|---|---|---|

| Basic budgeting and tracking; limited features. | Free | Students, individuals with simple financial needs. |

| More advanced features (e.g., investment tracking, budgeting tools); some features may be limited in the free version. | Freemium (Free basic version, paid for premium features) | Individuals who want more features but have a limited budget. |

| Comprehensive features, advanced analytics, and often priority support. | Subscription (Monthly or annual fee) | Families, freelancers, individuals with complex financial needs. |

Software Selection Based on User Needs: Best Personal Finance Software

Choosing the right personal finance software is like choosing the right pair of shoes – you wouldn’t wear hiking boots to a gala, would you? The perfect software depends entirely on your financial journey and aspirations. Selecting the wrong tool can lead to frustration and, dare we say, financial missteps. Let’s find the perfect fit for your financial footwear.

Different users have vastly different needs, and a one-size-fits-all approach simply won’t cut it in the world of personal finance software. Understanding your specific requirements is crucial to avoid ending up with a software package that’s either too basic or overly complex for your needs. Consider your financial goals, the complexity of your finances, and your comfort level with technology.

User Profiles and Software Requirements

To illustrate this point, let’s consider three distinct user profiles and their unique software needs. The differences highlight the importance of careful selection, ensuring you choose a tool that enhances your financial management, not hinders it.

| User Profile | Software Requirements | Example Software (Illustrative, not an endorsement) | Key Features |

|---|---|---|---|

| Beginner Investor | Simple interface, basic budgeting tools, tracking of investments (stocks, bonds, etc.), educational resources. | Personal Capital (simplified view), Mint | Easy-to-understand dashboards, investment tracking, basic reporting |

| Small Business Owner | Invoicing, expense tracking, tax reporting capabilities, integration with accounting software, robust reporting features. | QuickBooks Self-Employed, Xero | Expense categorization, invoicing, profit/loss reports, tax preparation assistance |

| High-Net-Worth Individual | Advanced portfolio management, tax optimization tools, net worth tracking, estate planning features, sophisticated reporting and analytics. | Quicken Premier, Wealthfront (for advisory services) | Complex asset tracking, tax-loss harvesting analysis, custom reporting, potential integration with financial advisors |

Data Import/Export Capabilities

The ability to seamlessly import and export data is paramount. Think of it as the software’s ability to speak different financial languages. You might start with one software and later switch, or you might need to share data with an accountant or financial advisor. A software package that doesn’t allow easy data transfer can become a major headache.

For example, if you’re switching from a spreadsheet to dedicated personal finance software, the ability to import your existing data (transactions, investments, etc.) is crucial to avoid tedious manual entry. Similarly, exporting data for tax preparation purposes is a must-have feature.

Reporting and Analytics Features

The reporting and analytics features of personal finance software are where the magic happens. They transform raw financial data into actionable insights, helping you understand your spending habits, track your progress toward financial goals, and make informed decisions. The sophistication of these features varies greatly depending on the software package.

| Software | Report Types | Data Visualization | Notes |

|---|---|---|---|

| Mint | Spending by category, net worth, budget vs. actual | Bar charts, pie charts | Simple, user-friendly |

| Quicken | Detailed transaction reports, investment performance, tax reports, budget analysis | Charts, graphs, customizable dashboards | More comprehensive, suitable for complex finances |

| Personal Capital | Investment performance, asset allocation, retirement planning projections | Interactive charts, graphs, portfolio visualizations | Strong focus on investment management |

| YNAB (You Need A Budget) | Budget progress, spending trends, forecasting | Visual budget representations, progress bars | Zero-based budgeting approach |

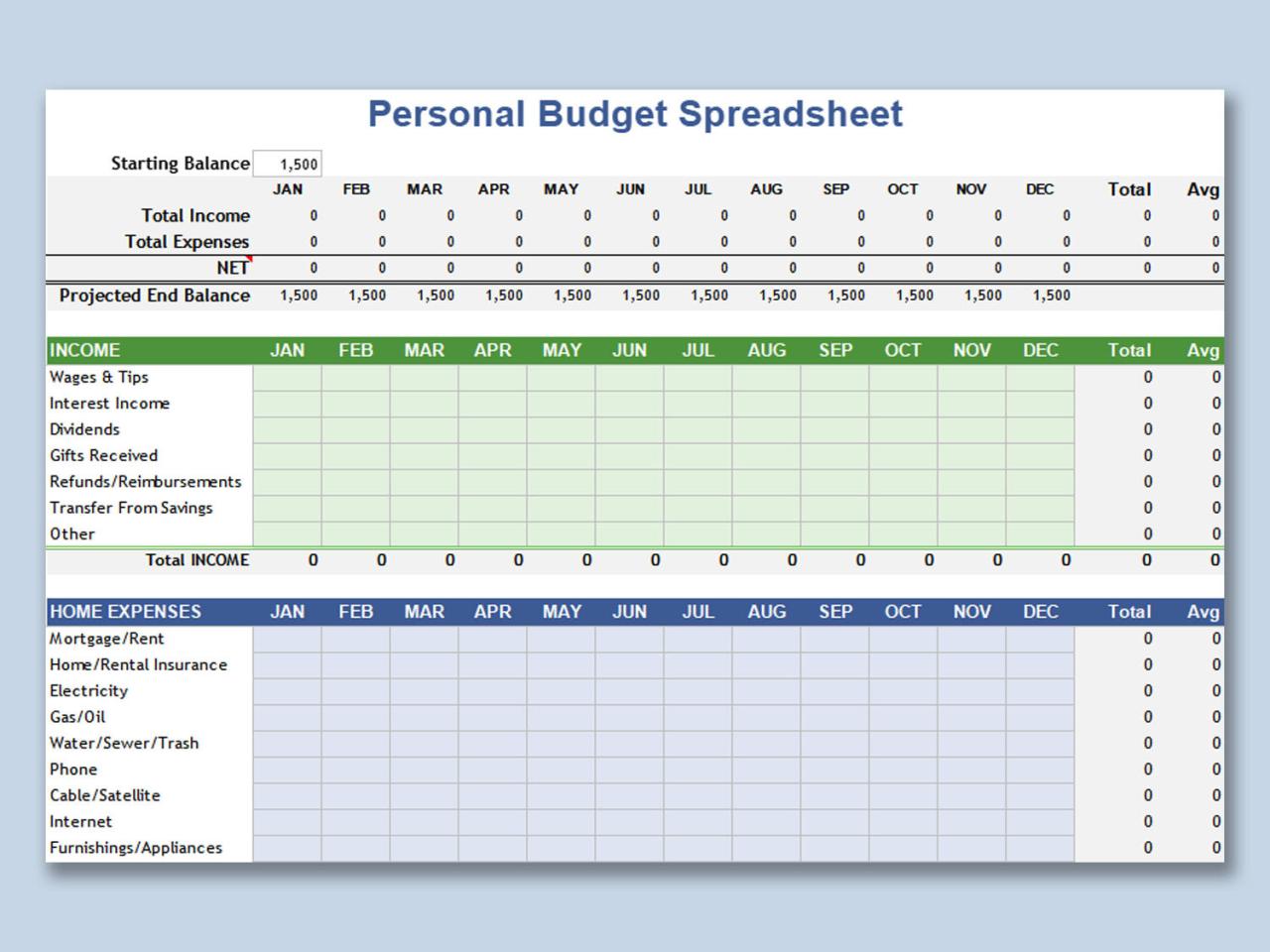

Utilizing Budgeting and Forecasting Tools

Budgeting and forecasting tools are the cornerstones of effective financial planning. These features allow you to set financial goals (e.g., saving for a down payment, paying off debt), track your progress, and anticipate future financial needs. Effective utilization requires discipline and a clear understanding of your financial situation.

For example, let’s say your goal is to save $20,000 for a down payment within two years. The budgeting tool allows you to allocate a specific amount each month towards this goal. The forecasting tool can then project how much you’ll have saved after a certain period, considering your current savings rate and anticipated income.

Regularly reviewing your budget and adjusting it as needed is crucial. Life throws curveballs, and your budget should be flexible enough to adapt to unexpected expenses or changes in income.

Evaluating Customer Reviews and Support

Choosing the right personal finance software is a bit like choosing a financial advisor – you want someone reliable, supportive, and (let’s be honest) not prone to sudden, inexplicable disappearances with your hard-earned cash. Customer reviews and support are crucial in making this decision, so let’s delve into the nitty-gritty.

Customer reviews, while seemingly straightforward, can be a minefield of biased opinions and cleverly disguised marketing ploys. Navigating this treacherous landscape requires a discerning eye and a healthy dose of skepticism.

Analyzing Customer Reviews

Understanding the context of a review is paramount. A five-star rave from someone who only used the software to track their Netflix spending might not be as insightful as a detailed critique from a seasoned budgeter. Look for reviews that offer specific examples, mentioning both positive and negative experiences. Beware of overly effusive praise with no concrete details; it might be a shill review. Consider the source – are the reviews clustered on a single platform, or spread across multiple reputable sites? A consistent pattern of positive (or negative) feedback across various platforms carries more weight. Additionally, consider the age of the reviews. Older reviews might reflect outdated software versions or customer support practices.

Customer Support Options

Personal finance software providers offer a variety of support options, each with its own pros and cons. Email support is often the most common, offering a written record of your interaction. Phone support allows for immediate assistance, but can be less efficient for complex issues. Online chat offers a blend of immediacy and a documented trail, but response times can vary. Some providers offer extensive FAQs or knowledge bases, acting as a self-service support option that can quickly resolve simple problems. The “best” option often depends on individual preference and the complexity of the issue. For example, a quick question about a specific feature might be best suited for online chat, while a complex problem requiring detailed explanation might be better addressed via email.

Software Provider Reputation and Track Record

A company’s reputation speaks volumes. A quick online search can reveal whether the provider has a history of data breaches, poor customer service, or questionable business practices. Look for independent reviews and ratings from reputable sources, not just those found on the company’s own website. Check for any news articles or blog posts mentioning the software or the company – this can provide a more balanced perspective than user reviews alone. A long-standing company with a proven track record of reliability is generally a safer bet than a newcomer with limited experience.

Customer Support Evaluation Rubric

To systematically evaluate customer support, consider this rubric:

| Criterion | Excellent | Good | Fair | Poor |

|---|---|---|---|---|

| Response Time | Within 1 business day | Within 2 business days | Within 3-5 business days | More than 5 business days or no response |

| Resolution Effectiveness | Issue resolved completely and efficiently | Issue resolved, but required multiple interactions | Partial resolution or workaround provided | Issue unresolved |

| Communication Clarity | Clear, concise, and professional communication | Mostly clear communication, minor ambiguities | Communication difficult to understand | Unclear, unprofessional, or unhelpful communication |

| Support Channels Availability | Multiple channels (email, phone, chat, etc.) available | Two or more channels available | One channel available | Limited or no support channels available |

Remember, selecting personal finance software is a serious undertaking – don’t let the allure of flashy features overshadow the importance of reliable support and a trustworthy provider.