Personal finance management aps – Personal finance management apps: They’re not just for spreadsheet-obsessed accountants anymore! From budgeting apps that whisper sweet nothings about saving to investing apps that bravely face the volatile stock market, these digital companions promise to tame your finances – or at least make the process slightly less terrifying. This exploration delves into the wild world of personal finance apps, examining their features, security, and overall impact on our increasingly complicated financial lives. Prepare for a journey filled with insightful analysis and, dare we say, a chuckle or two.

We’ll navigate the labyrinthine world of app features, comparing budgeting tools, investment platforms, and debt management solutions. We’ll also explore the crucial aspects of data security and privacy, because nobody wants their financial secrets splashed across the internet. Finally, we’ll peek into the future of personal finance apps, where artificial intelligence and blockchain technology might just revolutionize how we manage our money (or at least make it a bit more fun).

Defining Personal Finance Management Apps: Personal Finance Management Aps

Personal finance management apps: your digital financial Sherpas, guiding you through the sometimes treacherous terrain of budgeting, saving, and investing. These handy tools are more than just glorified calculators; they’re your personal financial assistants, striving to make your money work as hard as you do (hopefully harder!). They offer a range of features designed to simplify your financial life, helping you understand where your money goes and, more importantly, where it *could* go.

Personal finance management applications provide a centralized platform for tracking income, expenses, and assets. Core functionalities typically include secure data storage, customizable budgeting tools, transaction categorization, financial goal setting, and insightful reporting. Many apps also integrate with bank accounts and credit cards for automatic transaction imports, saving you the tedious manual entry of every latte purchase. Think of them as your friendly, ever-vigilant financial watchdogs, barking only when necessary (and hopefully not too often).

Categorization of Personal Finance Management Apps

The world of personal finance apps is diverse, catering to a wide range of financial needs and user sophistication. Apps can be broadly categorized based on their primary focus, each offering a unique set of features designed to address specific financial challenges.

- Budgeting Apps: These apps are the workhorses of personal finance management, helping users track income and expenses, create and monitor budgets, and identify areas for potential savings. Features often include customizable budget categories, spending visualizations (think colorful pie charts!), and alerts for exceeding budget limits. Mint and YNAB (You Need A Budget) are popular examples, each with its own approach to budgeting methodologies.

- Investing Apps: For those looking to grow their wealth, investing apps offer tools for managing investment portfolios, tracking performance, and researching investment opportunities. Some apps offer robo-advisors, providing automated portfolio management based on user risk tolerance and financial goals. Robinhood and Acorns are examples of apps that cater to different levels of investing experience, ranging from beginner-friendly to more sophisticated platforms.

- Debt Management Apps: Tackling debt can be daunting, but these apps can help streamline the process. Features often include debt tracking, repayment planning tools, and strategies for accelerating debt reduction. Many incorporate debt snowball or avalanche methods, providing visual progress reports to keep users motivated. While many budgeting apps include debt management features, some specialize in this area, providing more in-depth tools and strategies.

Target User Demographics

The ideal user for a personal finance app is anyone who wants more control over their finances. However, different apps target specific demographics based on their features and complexity.

| App Category | Target Demographic | Example Features |

|---|---|---|

| Budgeting Apps | Students, young professionals, individuals seeking to improve spending habits | Simple interface, basic budgeting tools, expense tracking, savings goals |

| Investing Apps | Individuals with some investment experience, those seeking long-term growth | Portfolio tracking, investment research, robo-advisor services, advanced charting |

| Debt Management Apps | Individuals with high-interest debt, those seeking to pay off debt quickly | Debt tracking, repayment planning, debt reduction strategies, budgeting tools |

App Features and Functionality Comparison

Choosing the right personal finance app can feel like navigating a minefield of budgeting brilliance and expense-tracking explosions. Fear not, intrepid saver! This section will dissect the features of some popular contenders, helping you choose the app that best suits your unique financial personality (are you a meticulous spreadsheet aficionado or a “winging-it” wonder?).

The following table compares three popular personal finance management apps. Remember, the best app is subjective and depends on individual needs and preferences. Think of this as a financial personality test, but with less inkblot interpretation.

Personal Finance App Feature Comparison

| App Name | Key Features | Pricing Model | User Reviews Summary |

|---|---|---|---|

| Mint | Budgeting, bill tracking, credit score monitoring, investment tracking. Provides a comprehensive overview of your financial life, often likened to a financial dashboard for your life. | Free (with optional paid features) | Generally positive, praised for its ease of use and comprehensive features. Some users report occasional glitches or difficulties linking accounts. |

| Personal Capital | Retirement planning tools, investment tracking, fee analysis, net worth calculation. Caters to a more sophisticated user base interested in investment management. | Free (with advisory services available for a fee) | Positive reviews from users who appreciate the advanced features and investment tracking capabilities. Some find the interface less intuitive than other apps. |

| YNAB (You Need A Budget) | Zero-based budgeting, goal setting, detailed transaction tracking. Focuses on mindful spending and achieving financial goals through a unique budgeting methodology. | Subscription-based | High praise for its effectiveness in helping users manage their money and achieve financial goals. Some users find the initial learning curve steep. |

Cloud-Based vs. Locally Stored Data

The age-old question: cloud or no cloud? For personal finance apps, this choice significantly impacts accessibility and security. Cloud-based apps offer the convenience of accessing your data from anywhere with an internet connection. However, this convenience comes with the risk of data breaches and reliance on a stable internet connection. Locally stored data keeps your information private but limits accessibility. Think of it as a digital vault versus a digital Swiss bank account – one is easily accessible, the other is more secure but less convenient.

Crucial Security Features in Personal Finance Apps

Security is paramount when entrusting your financial data to an app. Essential features include:

- Two-factor authentication (2FA): This adds an extra layer of security, requiring a code from your phone or email in addition to your password.

- Data encryption: This scrambles your data, making it unreadable to unauthorized individuals. Imagine your financial information as a top-secret recipe, only decipherable with the correct key.

- Regular security updates: These patches address vulnerabilities and keep your data safe from evolving threats. Think of these updates as your app’s financial bodyguard, always on alert.

- Robust fraud detection: This helps identify and prevent suspicious activity. It’s like having a financial watchdog, always keeping an eye out for potential problems.

User Experience and Interface Design

Designing a personal finance app isn’t just about crunching numbers; it’s about crafting a digital sanctuary where users can comfortably confront their finances without experiencing an existential crisis. A well-designed app should be as soothing as a warm cup of chamomile tea on a stressful Monday morning – not as terrifying as a tax audit. The key is intuitive navigation and visually appealing data representation, transforming the often-dreaded task of budget management into something almost… enjoyable.

A user-friendly interface is paramount. Imagine a world where managing your money is as easy as ordering a pizza online – that’s the goal. We need to ditch the confusing spreadsheets and replace them with a clean, modern design that even your grandma could navigate (after a brief tutorial, of course). This involves a careful balance of aesthetics and functionality, ensuring that the app is both visually pleasing and incredibly efficient. Think calming color palettes, clear typography, and a logical flow of information.

Intuitive Navigation and Data Visualization

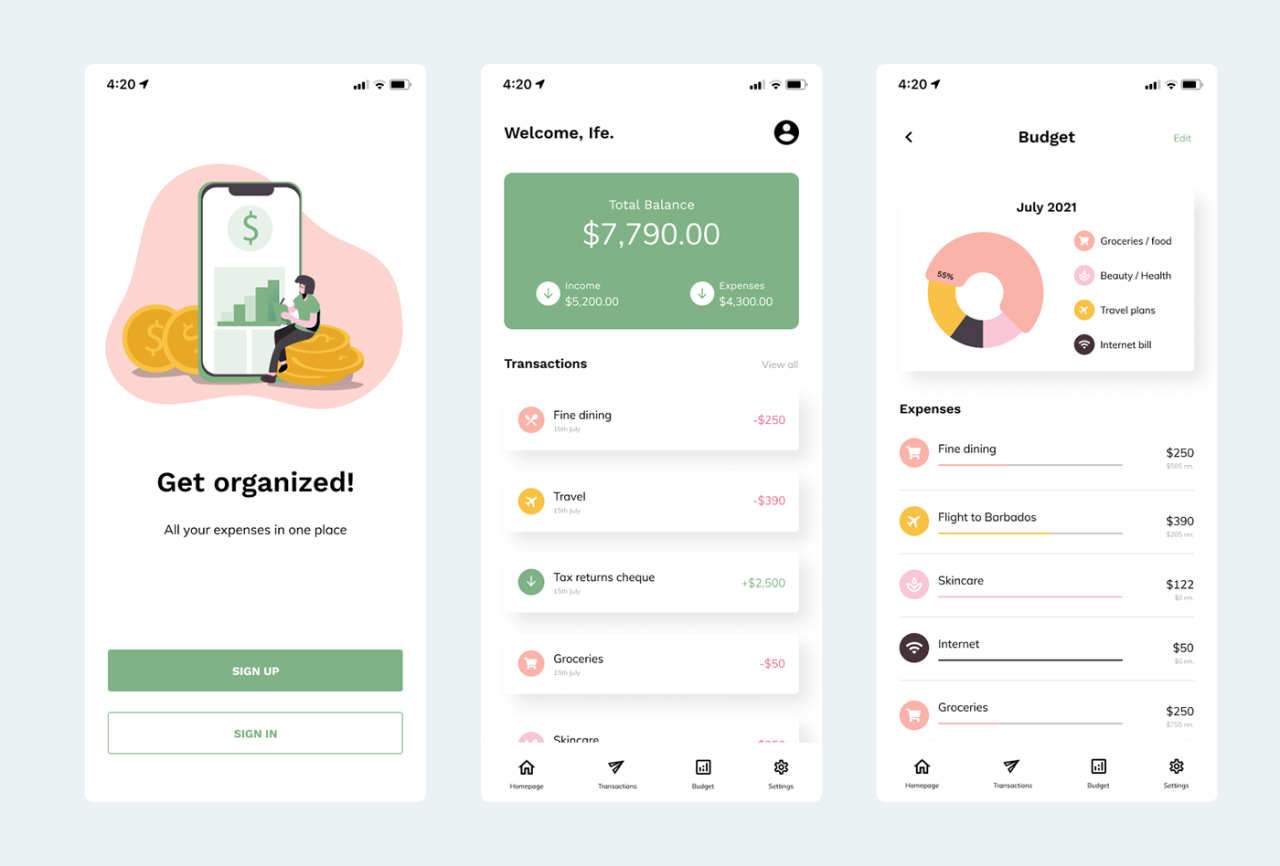

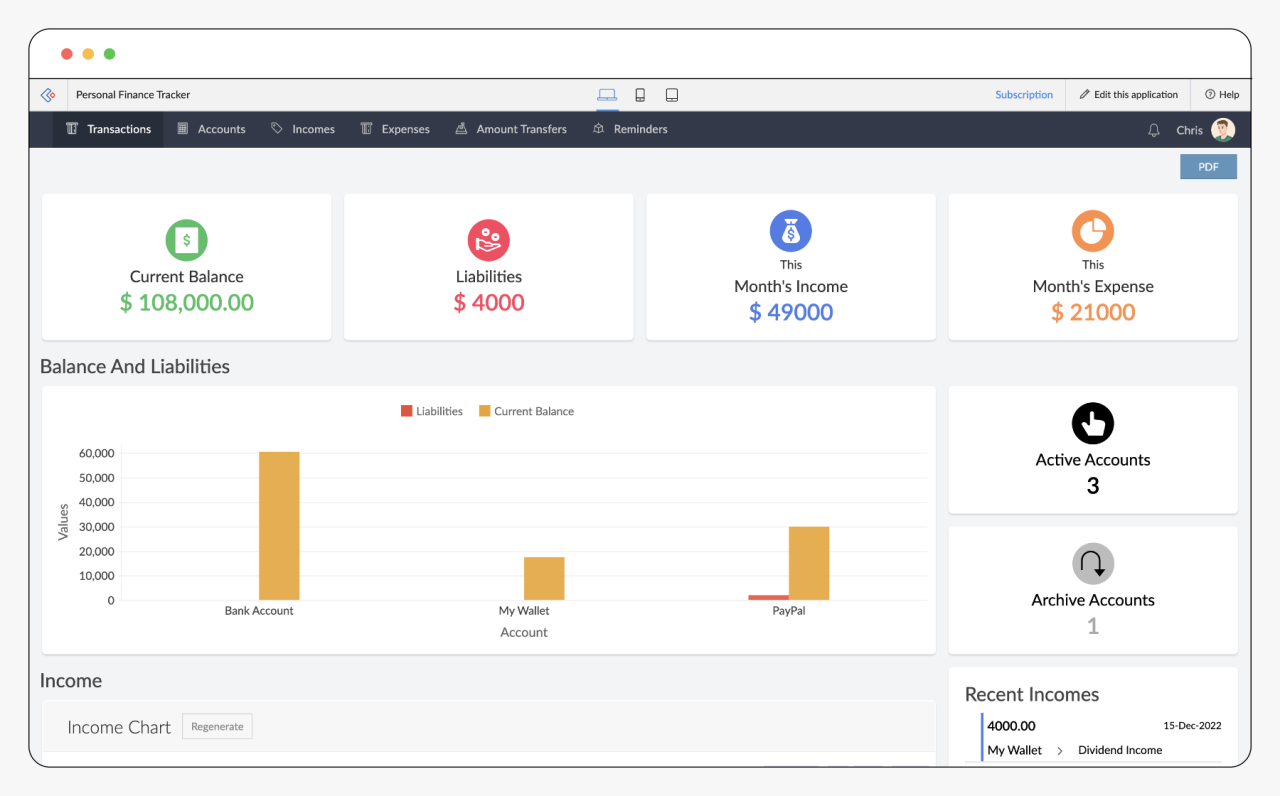

A mockup of our hypothetical personal finance app would feature a dashboard displaying key financial metrics at a glance. Think large, easily digestible charts showing spending categorized by type (e.g., groceries, entertainment, rent) and a clear overview of income and expenses for the current month and year. A circular progress bar indicating how much of the monthly budget has been spent would provide instant visual feedback. Navigation should be simple, using clear icons and labels for accessing different sections such as budgeting, transactions, goals, and reports. The overall aesthetic should be clean and uncluttered, avoiding overwhelming the user with unnecessary information. Imagine a dashboard resembling a well-organized control panel of a spaceship, not a chaotic junkyard of financial data.

Best Practices for Promoting Positive User Behavior

Encouraging positive financial habits requires more than just pretty visuals. Gamification can play a significant role. For example, awarding badges for reaching savings goals or consistently tracking expenses could incentivize users to engage with the app regularly. Progress bars visually demonstrate progress towards financial objectives, providing a sense of accomplishment. Furthermore, personalized financial insights and recommendations, based on spending patterns and goals, can help users make informed decisions and stay on track. Imagine a friendly virtual financial advisor offering gentle nudges and encouraging words, rather than a stern, judgmental accountant. Regular notifications reminding users to input transactions or check their budget can also help maintain consistent engagement.

User-Friendly Data Input Methods, Personal finance management aps

Efficient data input is crucial for an effective personal finance app. The app should seamlessly integrate with bank accounts to automatically import transaction data, minimizing manual input. However, manual entry should also be simple and intuitive. A well-designed interface could feature auto-complete functionality for common transactions and the ability to categorize expenses with simple tagging or pre-defined categories. Users should be able to easily edit or delete transactions if necessary. The process should be quick, effortless, and free of frustrating technical glitches. Think of it as the digital equivalent of a perfectly smooth, frictionless payment system. The easier it is to input data, the more likely users are to maintain accurate and up-to-date financial records.

Impact on Financial Literacy and Behavior

Personal finance management apps have the potential to revolutionize how we handle our money, but their impact extends far beyond simple budgeting. These digital assistants are quietly shaping our financial literacy and influencing our spending and saving habits, often in surprisingly effective (and sometimes hilariously unexpected) ways. Think of them as your ever-present, slightly judgmental, but ultimately helpful financial guru, residing conveniently on your phone.

These apps don’t just passively track expenses; they actively educate and nudge users toward better financial decisions. By providing clear visualizations of spending patterns, they unveil hidden spending habits that might otherwise remain unnoticed, leading to a greater awareness of personal finances. This increased awareness is the cornerstone of improved financial literacy. Moreover, the interactive nature of these apps makes learning about personal finance engaging and accessible, a far cry from the dry textbooks of yesteryear.

Gamification and Positive Financial Behaviors

Many personal finance apps incorporate gamification techniques to encourage positive financial behaviors. These techniques leverage the power of rewards and challenges to motivate users to stick to their budgets and achieve their financial goals. Imagine earning virtual badges for consistently saving money or receiving celebratory notifications for paying off debts. These seemingly small rewards can significantly impact long-term financial habits, making saving and budgeting feel less like a chore and more like a game. For example, some apps award points for completing tasks like tracking expenses or setting financial goals, which can then be redeemed for discounts or other incentives. Others use progress bars and visual representations to show users how close they are to achieving their targets, providing a constant source of motivation. The playful nature of these features can make the often-daunting process of financial management more engaging and enjoyable, encouraging sustained use and positive behavioral changes.

Comparison of App Features and Their Impact on User Financial Habits

The effectiveness of a personal finance app hinges on its features and how they influence user behavior. Different features can have both positive and negative consequences, and understanding these nuances is crucial for both app developers and users.

| Feature | Positive Impact | Negative Impact | Mitigation Strategies |

|---|---|---|---|

| Automated Budgeting | Reduces manual effort, provides clear overview of spending, promotes mindful spending. | Can feel restrictive, may not accommodate unexpected expenses, potential for over-reliance. | Allow for manual adjustments, incorporate flexibility features, provide educational resources on budgeting principles. |

| Expense Categorization | Identifies spending patterns, highlights areas for potential savings, facilitates informed decision-making. | Can be time-consuming if manual, inaccuracies in categorization can skew data, lack of personalized insights. | Offer automated categorization with manual override, provide clear categorization guidelines, integrate machine learning for improved accuracy. |

| Goal Setting and Tracking | Provides clear targets, enhances motivation, facilitates progress monitoring, builds financial discipline. | Can lead to disappointment if goals are unrealistic, lack of personalized guidance may hinder success, overemphasis on short-term goals. | Offer personalized goal recommendations, provide progress visualization, incorporate flexibility in goal adjustment, encourage long-term planning. |

| Debt Management Tools | Provides structured repayment plans, facilitates debt reduction, tracks progress, promotes financial responsibility. | Can be overwhelming for users with significant debt, lack of personalized advice may hinder effectiveness, potential for feelings of inadequacy. | Integrate financial counseling resources, provide personalized debt reduction strategies, offer motivational support, avoid judgmental language. |

")